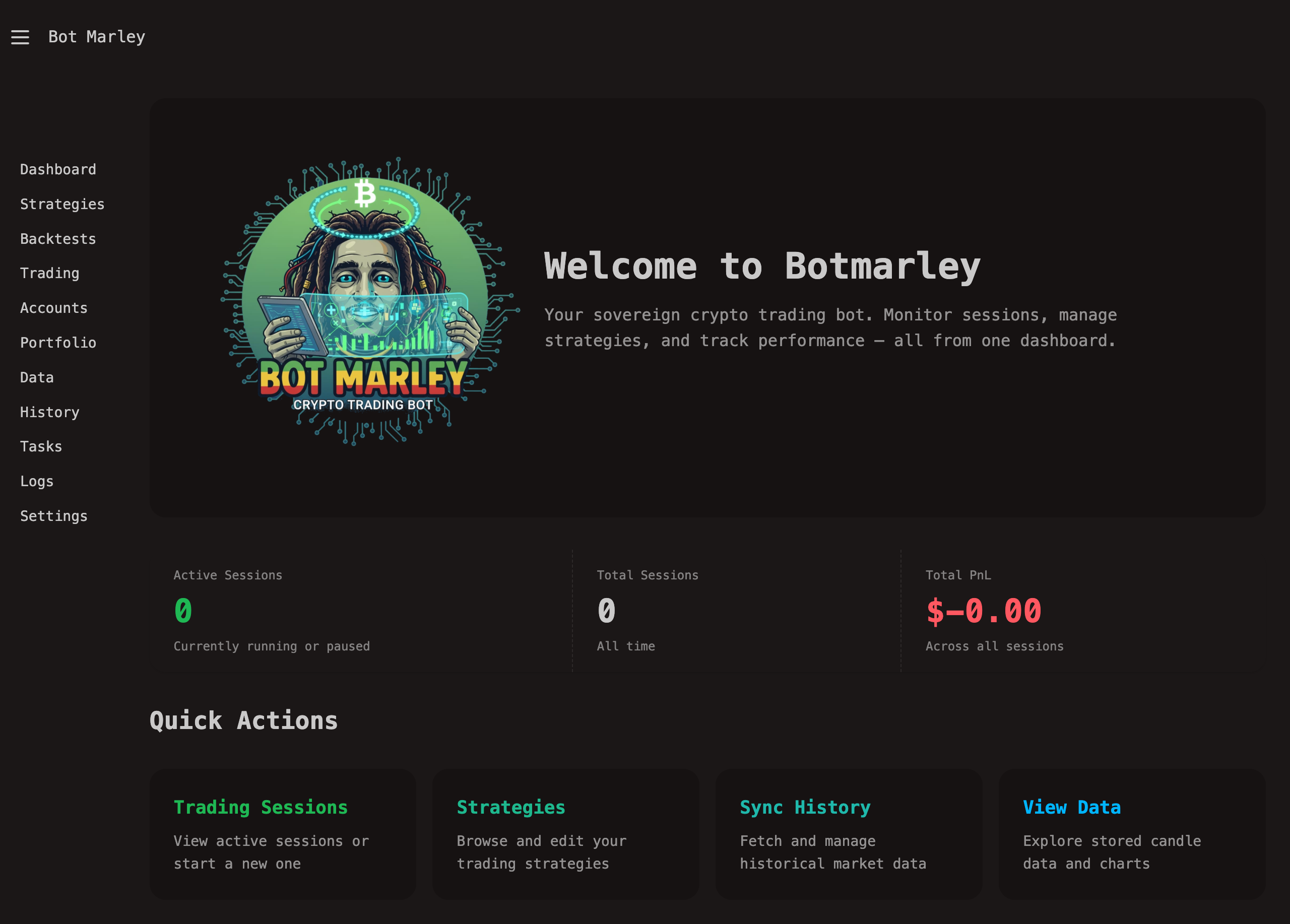

Welcome to Botmarley

Botmarley is a self-hosted, sovereign cryptocurrency trading bot built in Rust. It runs entirely on your own hardware, giving you full control over your trading strategies, API keys, and market data. No cloud services, no third-party access to your funds, no monthly subscriptions.

You install it, you run it, you own it.

Botmarley supports Kraken and Binance exchanges. It automatically detects which exchange to use based on your account type and trading pair.

What Botmarley Does

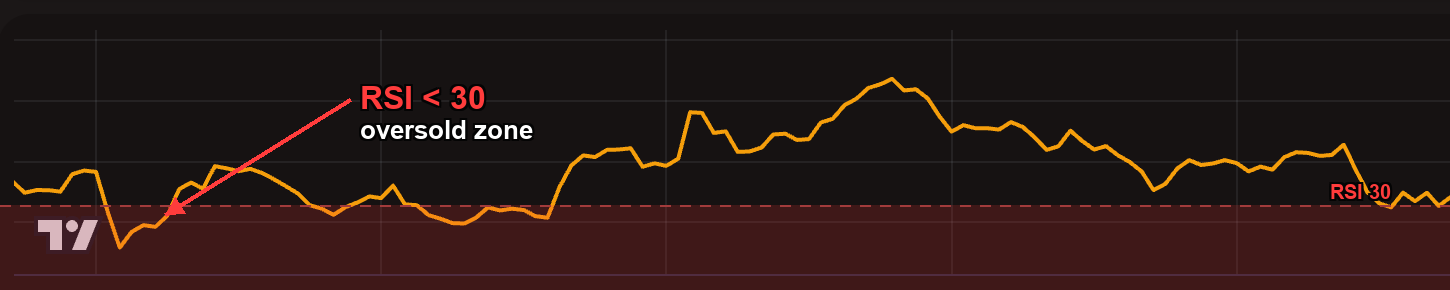

At its core, Botmarley automates cryptocurrency trading based on rules you define. You write a strategy that says things like "buy BTC when RSI drops below 30" or "sell 50% of my position when price rises 5% from entry," and Botmarley executes those rules 24/7 without you needing to watch charts.

Here is how the pieces fit together:

graph LR

Browser["Browser<br/>(Web Interface)"]

Bot["Botmarley<br/>(Trading Bot)"]

PG["PostgreSQL<br/>(Your Data)"]

Exchange["Exchange API<br/>(Kraken / Binance)"]

Browser <-->|"http://localhost:3000"| Bot

Bot <-->|"State & Logs"| PG

Bot <-->|"Market Data & Orders"| Exchange

- Browser -- You interact with Botmarley through a web interface at

http://localhost:3000. Pages update in real time as your bot trades. - Botmarley -- A blazing-fast trading engine built in Rust with Tokio and Axum. Handles strategy execution, order placement, data fetching, and serves a reactive web interface powered by HTMX.

- PostgreSQL -- Stores your accounts, trading sessions, backtest results, PnL history, activity logs, and configuration.

- Exchange API -- Botmarley connects to Kraken and Binance to fetch market data and place orders on your behalf.

Key Features

| Feature | Description |

|---|---|

| Dashboard | At-a-glance overview of active sessions, total PnL, and quick navigation to key areas. |

| Strategy Editor | Visual builder and raw TOML editor for defining trading rules. Real-time validation as you build. |

| Backtesting | Test strategies against historical data before risking real money. See PnL, trade count, win rate, and individual actions on a chart. |

| Live Trading | Execute strategies in real-time on Kraken and Binance. Start, pause, resume, and stop sessions. Live-updating charts with trade markers. |

| Accounts | Manage exchange API keys and paper (simulated) accounts. Each account is isolated. |

| Portfolio | Track total portfolio value over time in USD and BTC, with asset breakdowns per account. |

| Market Data | Download, browse, chart, and analyze historical candle data. Run indicators on stored data. |

| History Sync | Fetch historical 1-minute candles from your exchange. Derived timeframes (5m, 15m, 1h) are calculated locally. |

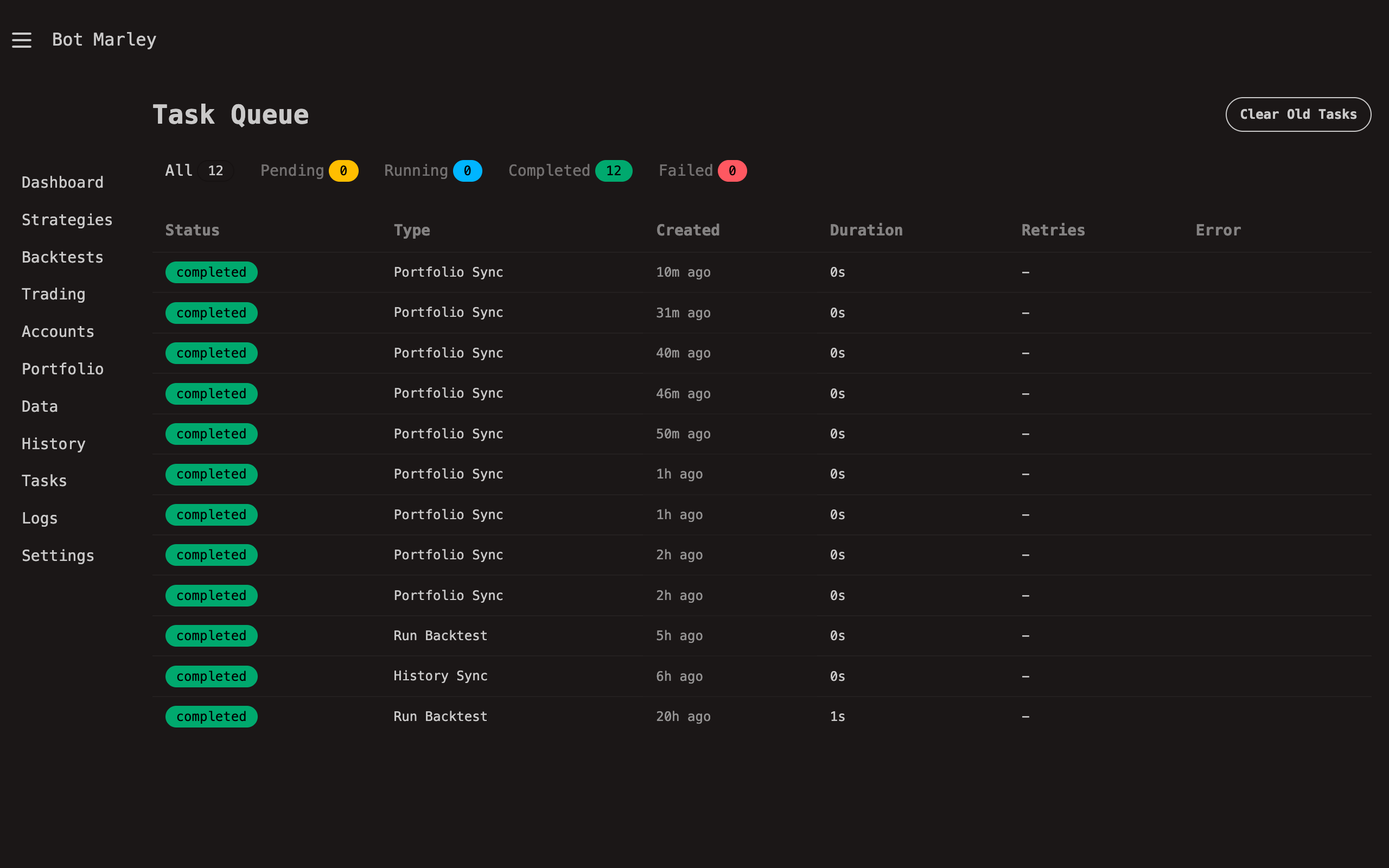

| Task Queue | Background job system for long-running operations like data sync and bulk backtests. |

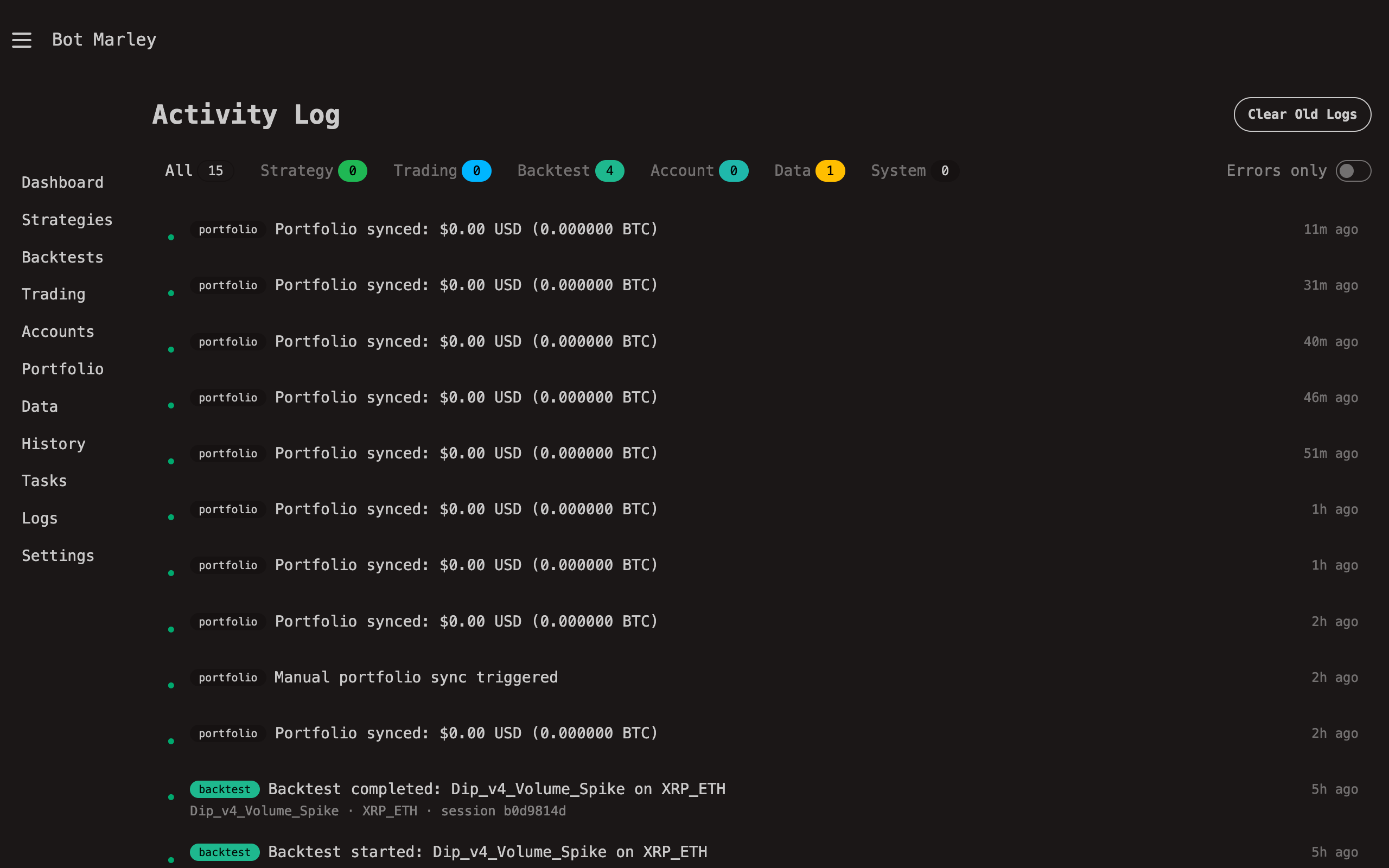

| Activity Logs | Detailed log of every action the bot takes, filterable by category (strategy, trading, backtest, account, data, system). |

| Settings | Configure server host/port, storage paths, active trading pairs, Telegram notifications, password protection, and UI themes. |

Who This Manual Is For

This manual is for cryptocurrency traders -- both beginners exploring automated trading for the first time and experienced traders who want full control over their bot.

- If you are new to trading bots, start with the Getting Started section. It walks you through installation, your first run, and a tour of every page.

- If you want to jump straight into building strategies, head to Strategies.

- If you are deploying Botmarley on a server, see Deployment.

You do not need any programming knowledge to use Botmarley. Strategies are defined in TOML files (a simple configuration format), and everything else is done through the web interface.

How to Use This Manual

The sidebar on the left organizes content into sections:

- Getting Started -- Installation, first run walkthrough, and a tour of the interface.

- Features -- Deep dives into each major feature: Dashboard, Accounts, Strategies, Backtesting, Live Trading, and Market Data.

- System -- Settings, task queue, activity logs, authentication, and Telegram integration.

- Deployment -- Running Botmarley locally and in production environments.

- Reference -- Strategy TOML specification, indicator reference, and glossary.

Use the search bar at the top to find specific topics. Each page is self-contained, so you can read them in any order.

Installation

This page walks you through installing Botmarley on your machine. By the end, you will have the bot running and accessible in your browser.

What You Need Before Starting

Botmarley is distributed as a pre-built binary. The only external dependency is PostgreSQL for data storage.

| Prerequisite | Why | How to check |

|---|---|---|

| PostgreSQL 15+ | Stores all bot state, trades, and logs. | psql --version |

The easiest way to run PostgreSQL is with Docker:

| Optional | Why | How to check |

|---|---|---|

| Docker | Run PostgreSQL in a container (no manual install). | docker --version |

| Docker Compose | Orchestrates the PostgreSQL container. | docker compose version |

If you already have PostgreSQL 15+ running on your system, you can use that instead of Docker. See the Environment Variables page for how to configure a custom database connection.

Installing Docker

If you do not have Docker installed:

macOS:

brew install --cask docker

Ubuntu/Debian Linux:

sudo apt update

sudo apt install docker.io docker-compose-v2

Windows:

Download and install Docker Desktop for Windows.

Download Botmarley

Download the latest release for your platform:

| Archive | Platform |

|---|---|

botmarley-arm64.tar.gz | Linux ARM64 — AWS Graviton, Raspberry Pi |

botmarley-amd64.tar.gz | Linux x86_64 — Most servers, Intel/AMD desktops |

botmarley-macos-arm64.tar.gz | macOS Apple Silicon (M1/M2/M3/M4) |

botmarley-windows-amd64.tar.gz | Windows x64 |

Not sure which one you need?

- Linux: Run

uname -m.aarch64→ ARM64,x86_64→ AMD64 - macOS: Use the Apple Silicon build (all modern Macs since late 2020)

- Windows: Use the Windows x64 build

Extract the Archive

Linux / macOS:

# Replace with your downloaded archive name

tar -xzf botmarley-arm64.tar.gz

cd botmarley

Windows (PowerShell):

tar -xzf botmarley-windows-amd64.tar.gz

cd botmarley

This creates the following files:

| Path | Purpose |

|---|---|

server (or server.exe on Windows) | The Botmarley binary |

templates/ | Web interface templates |

static/ | CSS, JavaScript, and images |

Initialize Botmarley

Before running for the first time, initialize the data directory:

Linux / macOS:

./server init

Windows (PowerShell):

.\server.exe init

This creates ~/.botmarley/ (or %USERPROFILE%\.botmarley\ on Windows) with:

- Default

settings.tomlconfiguration - Built-in trading strategies

- Example strategies for learning

- Data directories for market history

You only need to run init once. If the data directory already exists, the command will skip files that are already present and only add missing ones.

Start PostgreSQL

Botmarley stores all its state in PostgreSQL. The quickest way to get started is with Docker:

docker run -d \

--name botmarley-db \

-e POSTGRES_USER=botmarley \

-e POSTGRES_PASSWORD=botmarley_dev \

-e POSTGRES_DB=botmarley \

-p 5432:5432 \

postgres:17

If you prefer Docker Compose, create a docker-compose.yml with a postgres service, or use the one from the Production Deployment guide.

Verify the database is running:

docker ps | grep botmarley-db

Run Botmarley

Linux / macOS:

./server

Windows (PowerShell):

.\server.exe

Botmarley initializes the database schema on first run and starts listening on port 3000.

Verify the Installation

Open your browser and navigate to:

http://localhost:3000

You will see the license setup page. Follow the instructions in First Run to configure your API key and start trading.

If you see a connection error, check that:

- PostgreSQL is running:

docker ps - The server started without errors in the terminal

- Port 3000 is not already in use by another application

Stopping Botmarley

To stop the server, press Ctrl+C in the terminal where it is running.

To stop PostgreSQL:

docker stop botmarley-db

Your PostgreSQL data persists inside the Docker volume. Running docker stop keeps your data. To wipe the database and start fresh, run docker rm botmarley-db and create a new container.

Next Steps

With Botmarley running, continue to First Run for a guided walkthrough of the initial setup — including license activation and exchange configuration.

First Run

You have Botmarley installed and running at http://localhost:3000. This page walks you through the essential first-time setup: configuring settings, adding an account, downloading market data, creating a strategy, and running your first backtest.

By the end, you will have tested a strategy against historical data without risking any real money.

graph LR

A["1. Settings"] --> B["2. Add Account"]

B --> C["3. Download Data"]

C --> D["4. Create Strategy"]

D --> E["5. Run Backtest"]

When you open http://localhost:3000 for the first time, you will see the main dashboard. This is your starting point for everything that follows.

License Setup

Botmarley requires an API key to unlock all features.

- Visit lipinski.work to request your API key

- Open Settings in the Botmarley web interface

- Enter your API key in the License section

- Click Save

Botmarley validates your key immediately. Once validated, all features become available.

Without a valid key, only the Settings page is accessible.

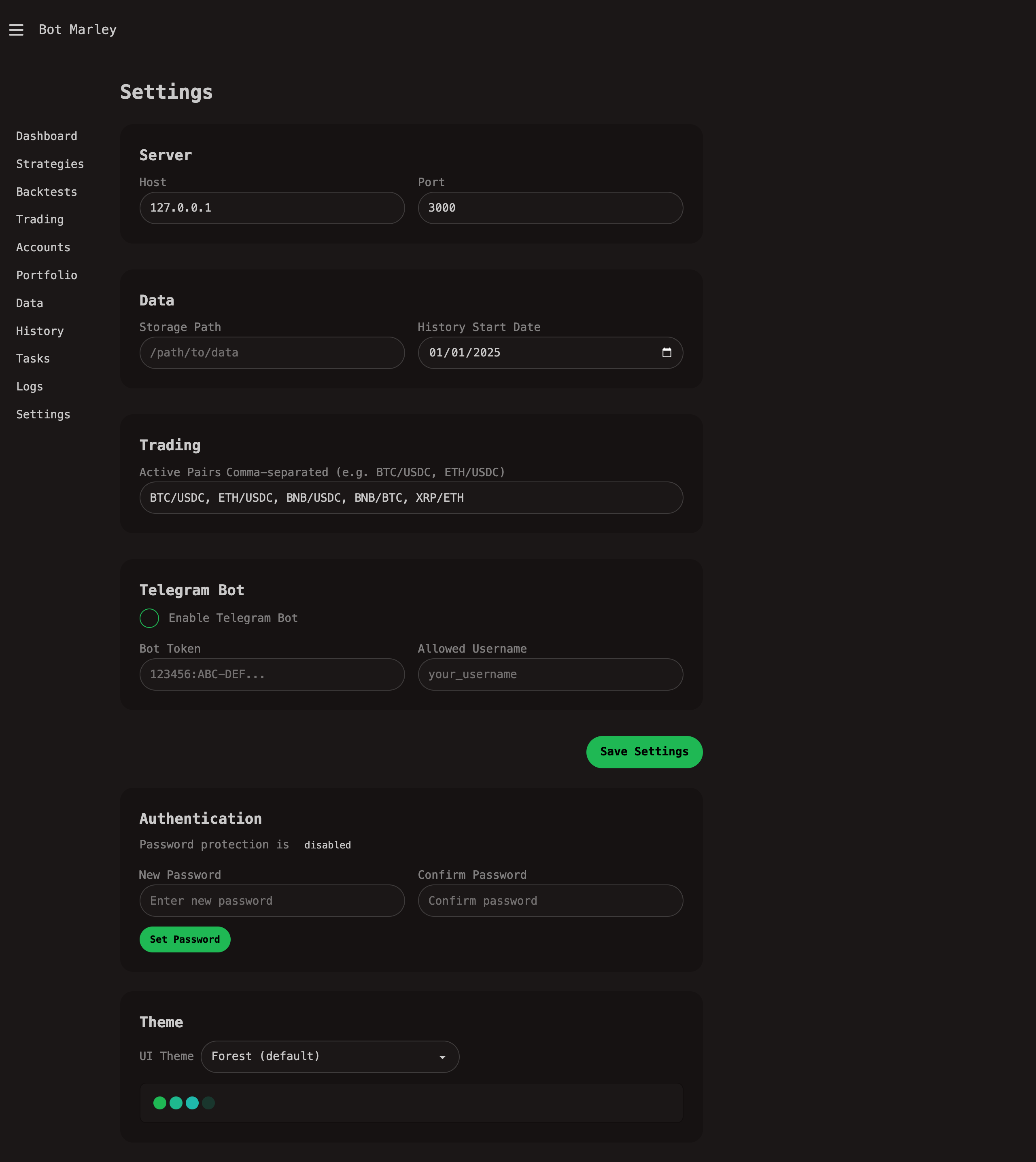

Step 1: Configure Settings

Navigate to Settings in the sidebar (or go to http://localhost:3000/settings).

The Settings page has several sections. For your first run, focus on these:

Trading Pairs

In the Trading card, set your Active Pairs. These are the cryptocurrency pairs you want to trade and download data for. Enter them comma-separated in the format BASE/QUOTE:

BTC/USDC, ETH/USDC

Start with one or two pairs. You can always add more later. BTC/USDC is a good starting point because it has the most historical data and liquidity.

Data Storage

The Storage Path tells Botmarley where to save Arrow files (historical candle data). The default path works for most setups. If you want to store data on a different drive, change it here.

History Start Date

Set History Start Date to control how far back Botmarley fetches historical data. A reasonable starting point is 6-12 months ago. The more history you have, the more thorough your backtests will be, but downloading takes longer.

Save

Click Save Settings at the bottom. A green success banner confirms your settings were saved.

You can skip the Telegram Bot and Authentication sections for now. They are useful for production deployments but not required for getting started.

Step 2: Add Your First Account

Navigate to Accounts in the sidebar.

Click the Add Account button. A modal dialog appears with these fields:

| Field | What to enter |

|---|---|

| Name | A friendly name, e.g., "Paper Trading" |

| Description | Optional, e.g., "For testing strategies" |

| Account Type | Select Paper (Simulated) |

A paper account simulates trades without connecting to any exchange. No API keys are needed. This is the safest way to learn how Botmarley works.

Click Create to save the account.

Do not use a live exchange account with real API keys until you are comfortable with how strategies behave. Always test with a paper account first.

When You Are Ready for Live Trading

When you eventually want to trade with real funds, create a new account with:

- Account Type: Kraken or Binance

- API Key and API Secret: Generated from your exchange account (see Managing Accounts for step-by-step instructions for each exchange)

Your API keys are stored locally in Botmarley's PostgreSQL database. Never share your API secret. When generating keys on your exchange, grant only the permissions you need (query funds, create orders) and avoid granting withdrawal permissions.

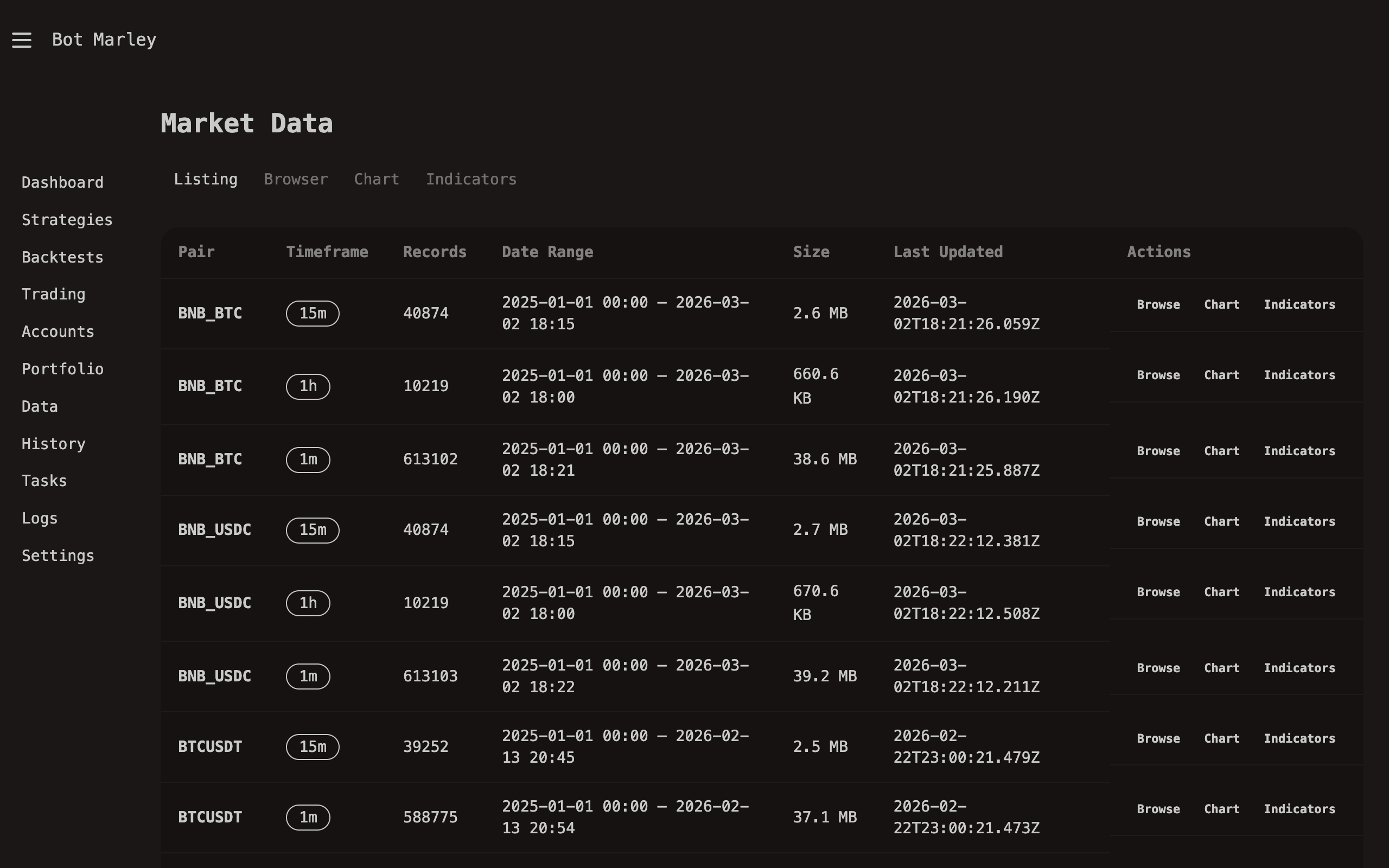

Step 3: Download Market Data

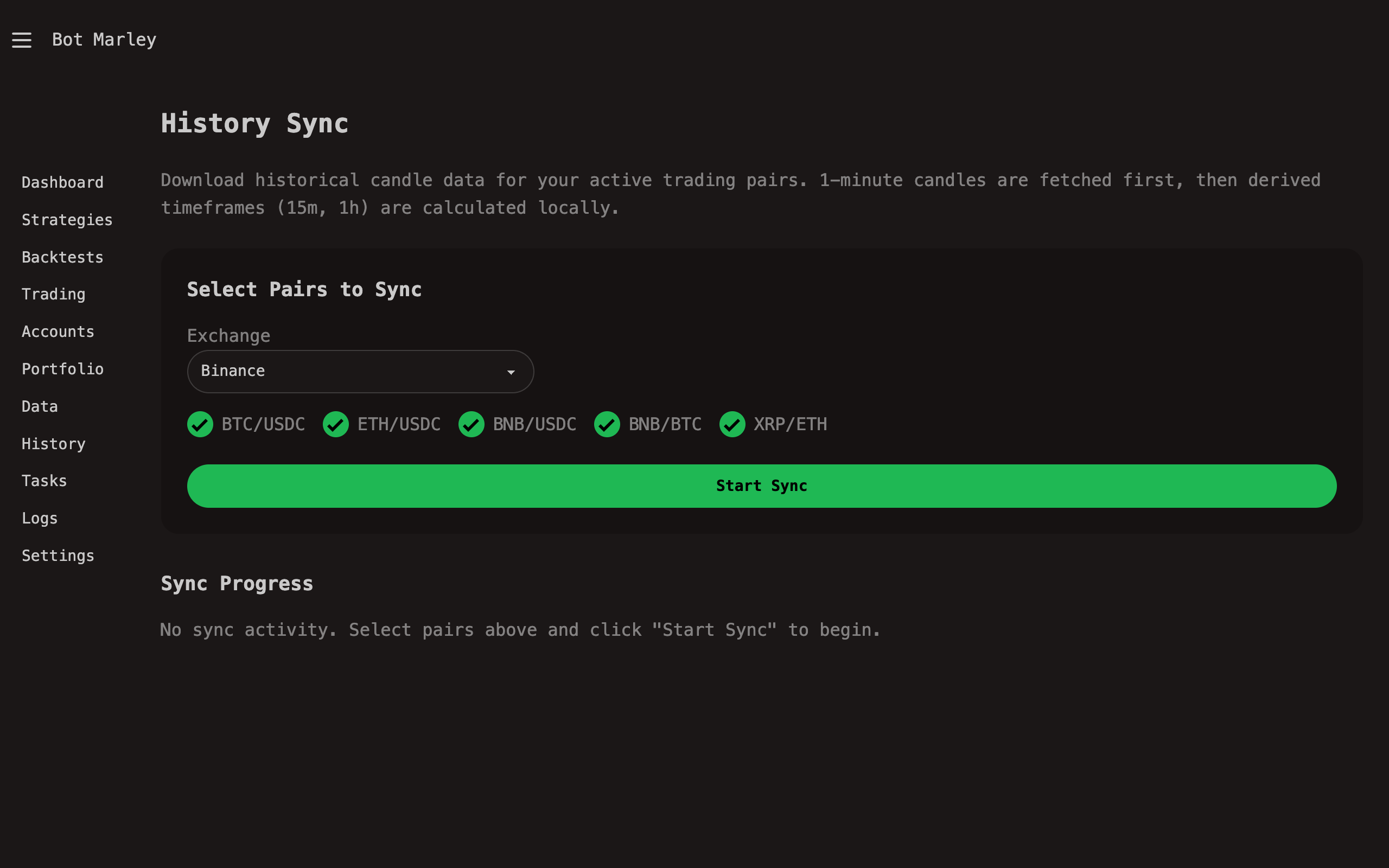

Navigate to History in the sidebar.

Before you can backtest, Botmarley needs historical candle data. The History Sync page lets you download it from Kraken or Binance.

- Select an exchange (Kraken or Binance) in the dropdown.

- Your active pairs (configured in Settings) appear as checkboxes. Make sure the pairs you want are checked.

- Click Start Sync.

Botmarley downloads 1-minute candles from the selected exchange and stores them in Apache Arrow format. This runs as a background task -- you can watch progress on the same page, which auto-refreshes every 2 seconds.

The initial download can take several minutes depending on how far back your history start date is. Subsequent syncs are incremental -- they only fetch new candles since the last sync.

Once the sync completes, navigate to Data in the sidebar to verify. You should see entries in the table showing your pairs, the number of records, date range, and file size.

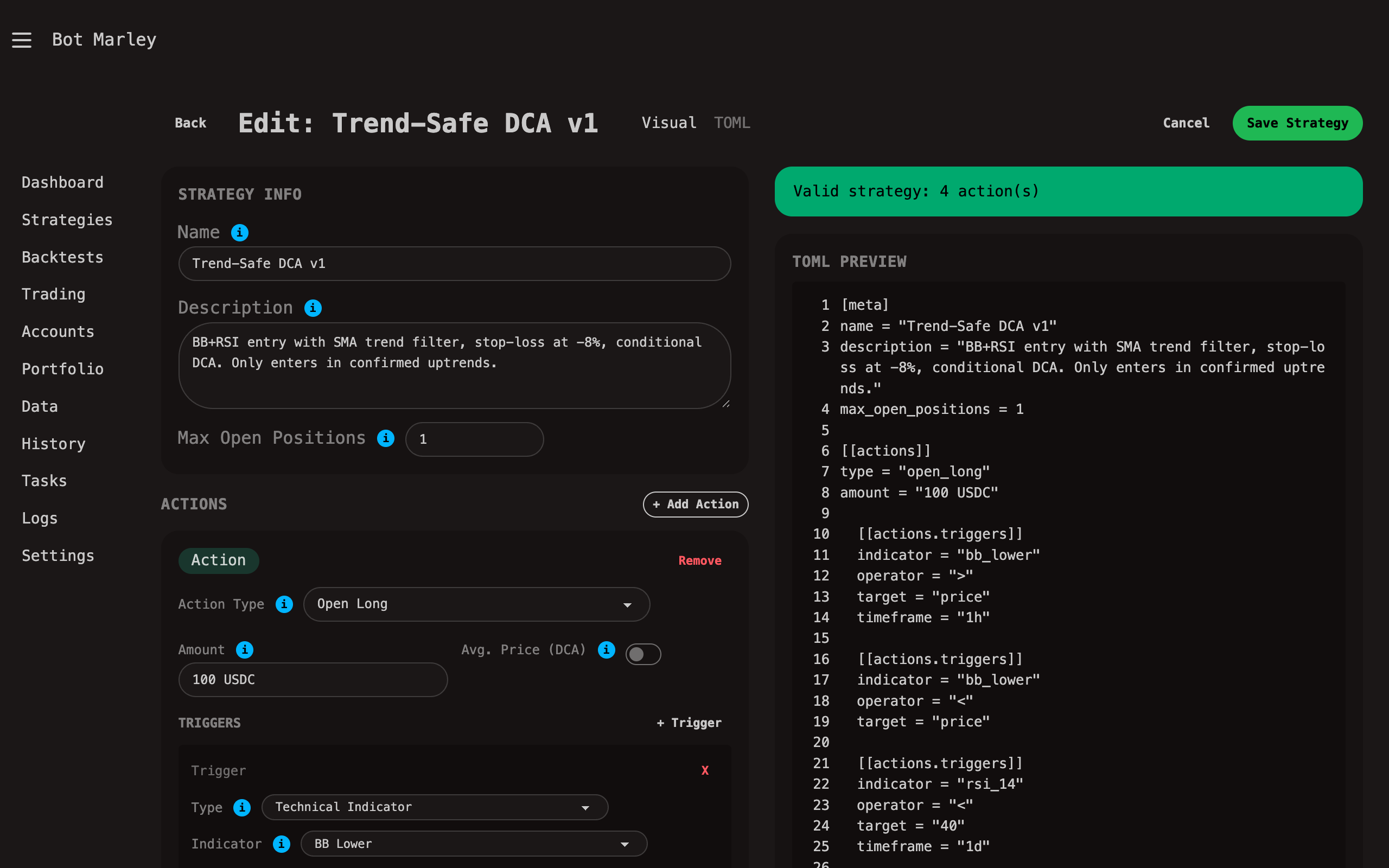

Step 4: Create Your First Strategy

Navigate to Strategies in the sidebar and click + New Strategy.

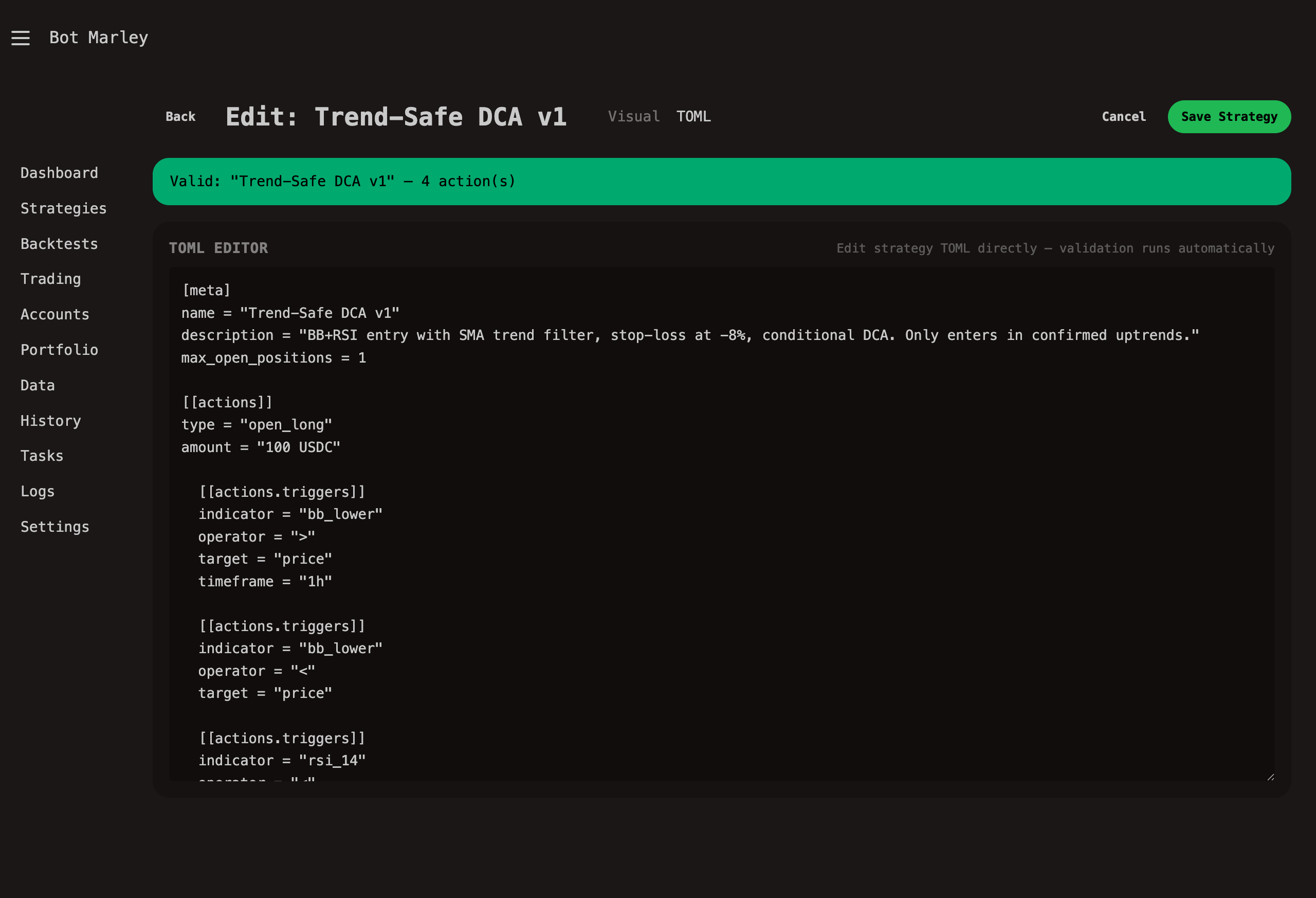

The Strategy Editor opens with two modes:

- Visual (default) -- A form-based builder with dropdowns and input fields.

- TOML -- A raw text editor for the strategy configuration file.

For your first strategy, use the Visual mode. Here is a simple RSI-based strategy to start with:

Strategy Info

- Name:

RSI Bounce - Description:

Buy when RSI is oversold, sell when overbought - Max Open Positions:

1

Action 1: Open Long

Click + Add Action, then configure:

- Action Type: Open Long

- Amount:

100 USDC

Now add a trigger: Click + Trigger within this action.

- Type: Technical Indicator

- Indicator: RSI 14

- Operator: Less Than (<)

- Target:

30 - Timeframe: 1h

This means: "Open a long position worth 100 USDC when the 1-hour RSI(14) drops below 30."

Action 2: Sell

Click + Add Action again:

- Action Type: Sell

- Amount:

100%

Add a trigger:

- Type: Technical Indicator

- Indicator: RSI 14

- Operator: Greater Than (>)

- Target:

70 - Timeframe: 1h

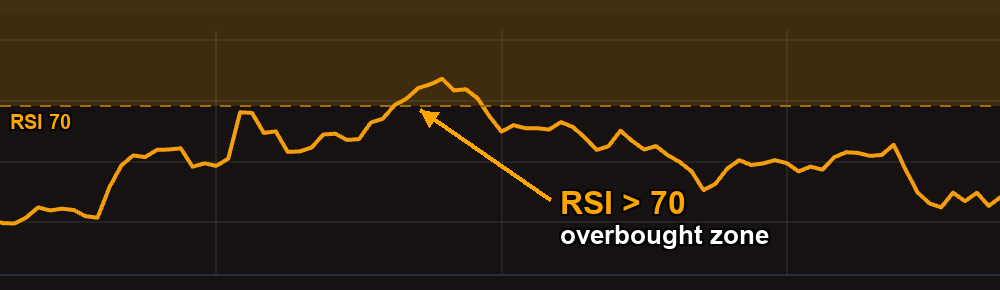

This means: "Sell the entire position when the 1-hour RSI(14) rises above 70."

Validate and Save

As you build, the right panel shows a live TOML Preview of your strategy and a validation status. It should show a green "Valid strategy: 2 action(s)" banner.

The generated TOML looks like this:

[meta]

name = "RSI Bounce"

description = "Buy when RSI is oversold, sell when overbought"

max_open_positions = 1

[[actions]]

type = "open_long"

amount = "100 USDC"

[[actions.triggers]]

indicator = "rsi_14"

operator = "<"

target = "30"

timeframe = "1h"

[[actions]]

type = "sell"

amount = "100%"

[[actions.triggers]]

indicator = "rsi_14"

operator = ">"

target = "70"

timeframe = "1h"

Click Save Strategy to store it.

Step 5: Run Your First Backtest

Go back to the Strategies list. You should see "RSI Bounce" in the table. Click the Backtest button on its row.

A modal dialog appears asking for:

| Field | What to enter |

|---|---|

| Pair | Select a pair you downloaded data for (e.g., BTC/USDC) |

| Initial Capital | 10000 (USD) |

| Start Date | The start of your downloaded data range |

| End Date | The end of your downloaded data range |

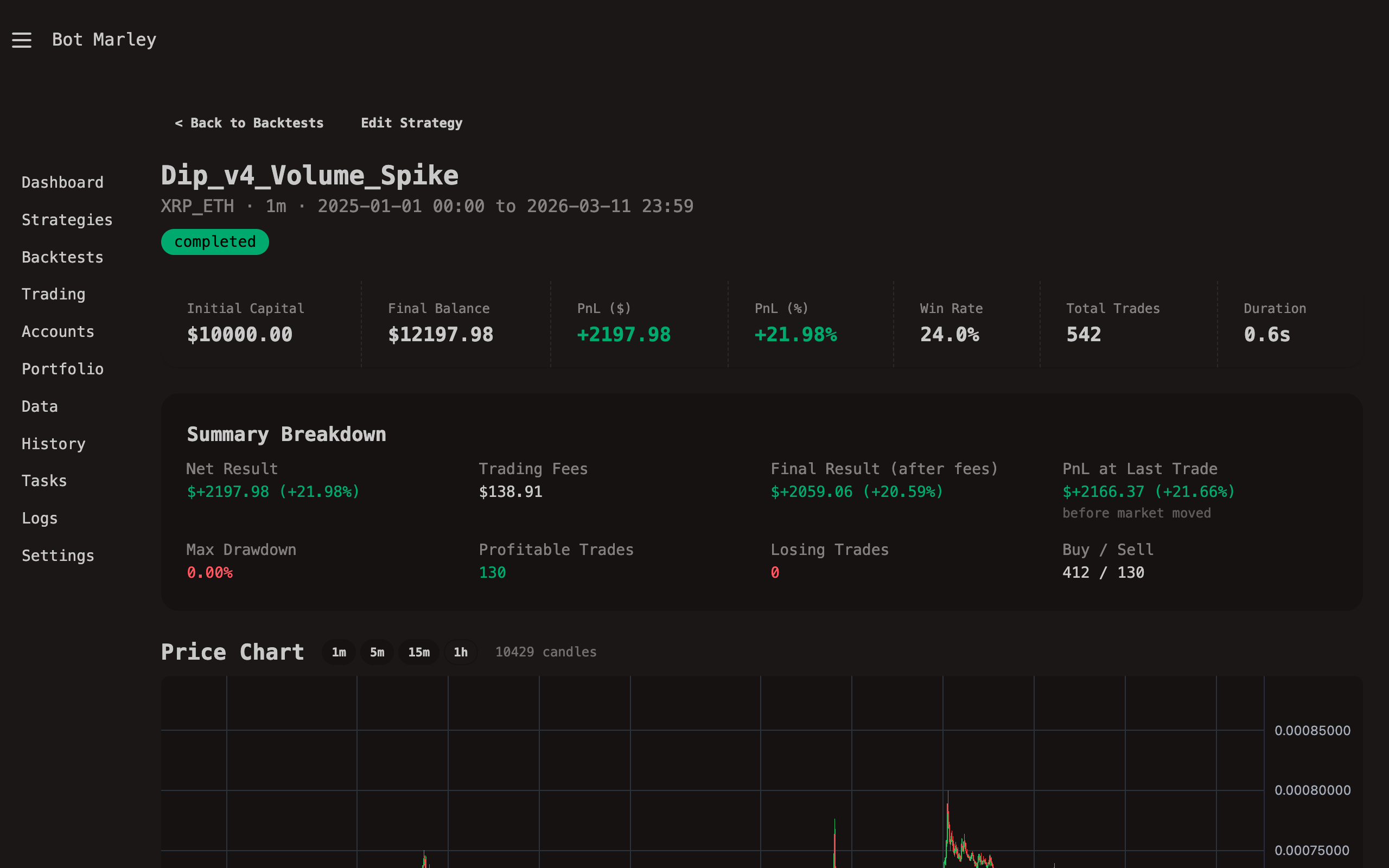

Click Run Backtest. Botmarley runs the strategy against the historical data and redirects you to the Backtests page.

Find your backtest in the list and click View to see the results:

- PnL -- Total profit or loss in dollars and as a percentage.

- Trade count -- How many buy/sell actions were executed.

- Win rate -- Percentage of profitable trades.

- Chart -- A candlestick chart with trade markers showing where each action occurred.

- Actions table -- A detailed log of every trade with timestamps, prices, and amounts.

Your first strategy probably will not be profitable -- and that is perfectly fine. Backtesting is about learning and iterating. Go back to the Strategy Editor, adjust the RSI thresholds or add additional triggers, and run another backtest. Repeat until you find settings that produce results you are comfortable with.

What to Do Next

You now understand the core workflow: settings, accounts, data, strategies, backtesting. From here:

- Quick Tour -- Walk through every page in the interface.

- Strategies -- Learn about all the trigger types, indicators, and strategy patterns.

- Backtesting -- Understand backtest results in depth and run bulk backtests.

- Live Trading -- When you are ready, start a live session with a paper, Kraken, or Binance account.

Quick Tour

This quick tour walks you through every major section of Botmarley so you know where everything lives.

Navigation

The sidebar on the left provides access to all sections:

| Section | What It Does |

|---|---|

| Dashboard | Portfolio overview and active session status |

| Accounts | Manage exchange connections |

| Portfolio | Track total portfolio value over time |

| Strategies | Create and edit trading strategies |

| Backtesting | Test strategies against historical data |

| Trading | Run live trading sessions |

| Data | Download and browse market data |

| Tasks | View background job queue |

| Logs | Activity and event history |

| Settings | Application configuration |

Dashboard

The dashboard (/) shows a summary of your portfolio value and any active trading sessions. It's your home base for monitoring at a glance.

Accounts

Navigate to Accounts to connect your Kraken or Binance exchange account or create a Paper (simulated) account for testing. Each account stores API credentials securely and can be verified with a balance check.

Strategies

The Strategies section lets you create, edit, and manage trading strategies defined in TOML format. Each strategy consists of:

- Actions — buy/sell operations, each with their own trigger conditions

- Indicators — technical analysis tools (SMA, EMA, RSI, Bollinger Bands, MACD, OBV, OBV-SMA, TTM Trend, StochRSI, ROC, ATR, Vol SMA, Price)

- Position management — DCA settings, max open positions, allocation percentages

Backtesting

Before going live, test your strategies against historical data in the Backtesting section. You'll see:

- Profit/Loss (absolute and percentage)

- Win rate and trade count

- Maximum drawdown

- An interactive chart showing entries and exits

Live Trading

When you're confident in a strategy, start a Trading Session. Select an account, a strategy, and a trading pair, then hit Start. You can:

- Pause — temporarily halt execution

- Resume — continue from where you paused

- Stop — end the session permanently

Real-time updates stream via SSE (Server-Sent Events), so the page updates automatically.

Market Data

The Data section lets you download historical candle data from Kraken or Binance. Data is stored in Apache Arrow format for fast access. You can browse downloaded datasets and run indicator calculations.

Settings

Configure application-wide settings including:

- Server host and port

- Telegram bot notifications

- Password protection

- Data storage paths

What's Next?

Now that you know the layout, dive into the specific sections that interest you most. We recommend starting with Accounts to set up your first connection, then exploring Strategies to build your first trading strategy.

Dashboard

The Dashboard is your home page — the first thing you see when you open Botmarley at http://localhost:3000.

What You'll See

The dashboard provides a high-level overview of your trading operation:

Portfolio Summary

If you have accounts connected and portfolio sync running, you'll see:

- Total Portfolio Value (USD) — combined value across all accounts

- Total Portfolio Value (BTC) — your holdings measured in Bitcoin

- BTC Price — current Bitcoin price in USD

- Last Sync — when portfolio data was last refreshed

Active Trading Sessions

Any currently running or paused trading sessions appear here with:

- Session name and trading pair

- Current status (Running, Paused)

- Profit/Loss so far

- Number of actions executed

Click on any active session to jump directly to its detail page with real-time charts and controls.

Empty State

If this is your first time using Botmarley, the dashboard will show helpful links to get started:

- Add an Account — connect to Kraken or create a Paper account

- Create a Strategy — build your first trading strategy

- Download Data — fetch historical market data for backtesting

Auto-Refresh

The dashboard uses HTMX polling to stay up-to-date. Active session stats refresh automatically without needing to reload the page.

Navigation

From the dashboard, you can quickly navigate to any section using the sidebar. The most common workflows from here:

graph LR

D[Dashboard] --> A[Accounts]

D --> S[Strategies]

D --> T[Trading]

D --> B[Backtesting]

A --> T

S --> B

B --> T

This flow represents the typical journey: set up accounts, create strategies, backtest them, then go live.

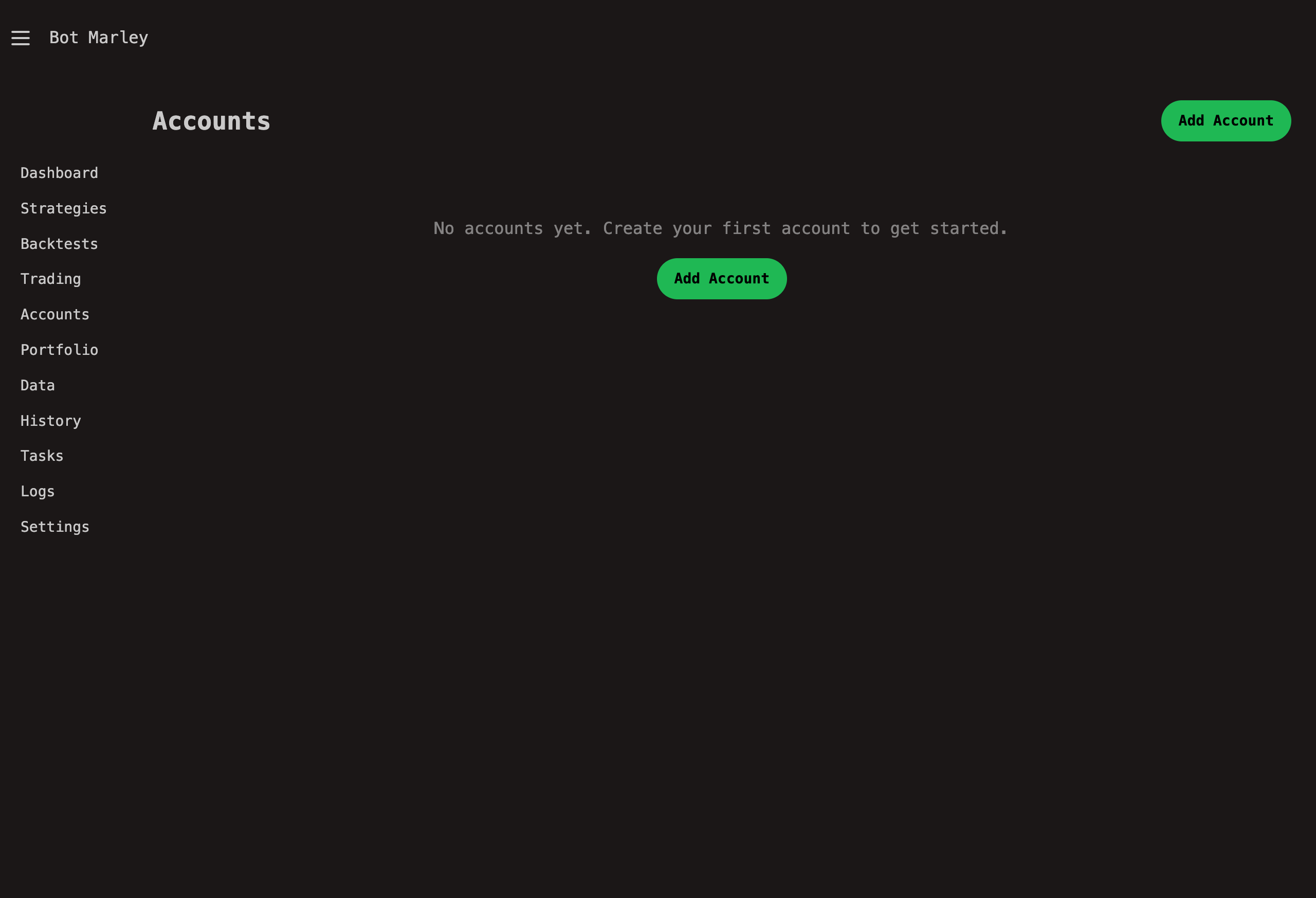

Accounts

Accounts are the bridge between Botmarley and the outside world. Every action the bot takes -- whether it is placing a live trade on an exchange or simulating one locally -- happens through an account. Before you can backtest a strategy, run a live session, or track a portfolio, you need at least one account configured.

What Is an Account?

An account in Botmarley represents a single source of funds. It stores:

- Name and description -- a human-readable label you choose (e.g. "My Kraken Spot" or "Paper Testing").

- Account type -- determines whether the account connects to a real exchange or runs in simulation.

- API credentials -- only required for real exchange accounts.

- Verification status -- tells you whether Botmarley has successfully tested the credentials.

- Assets -- the token balances held in that account (BTC, ETH, USD, etc.).

You can have as many accounts as you like. A common setup is one Paper account for testing and one Kraken account for live trading.

Account Types

Botmarley supports three account types. Each behaves differently with respect to credentials, verification, and trading.

Paper (Simulated)

| Property | Value |

|---|---|

| Requires credentials | No |

| Connects to exchange | No |

| Verification status | Always "N/A" |

Paper accounts are purely local. No money leaves your machine, and no API calls are made to any exchange. Paper accounts are ideal for:

- Learning how Botmarley works without financial risk.

- Testing a new strategy before going live.

- Running backtests against historical data.

When you create a Paper account, Botmarley assigns it a starting balance that you can adjust manually. Trades executed against a Paper account update its local balances but never touch a real order book.

Start with a Paper account. You can always add a real exchange account later once you are comfortable with how your strategies behave.

Kraken (Real Exchange)

| Property | Value |

|---|---|

| Requires credentials | Yes (API key + secret) |

| Connects to exchange | Yes -- Kraken REST + WebSocket APIs |

| Verification status | Must be verified before use |

Kraken accounts connect Botmarley to your real Kraken exchange account using API credentials that you generate on Kraken's website. Once verified, Botmarley can:

- Sync balances -- pull your current holdings from Kraken.

- Place orders -- execute buy/sell orders during live trading sessions.

- Fetch market data -- download candle history via the Kraken REST API.

You control what Botmarley is allowed to do by setting the appropriate API key permissions on Kraken (see the Managing Accounts chapter for details).

A Kraken account operates with real money. Double-check your strategy in Paper mode before pointing it at a Kraken account.

Binance

| Property | Value |

|---|---|

| Requires credentials | Yes (API key + secret) |

| Connects to exchange | Yes |

| Verification | HMAC-SHA256 signed request to /api/v3/account |

A Binance account connects to the Binance exchange using your API key and secret. Botmarley supports:

- Verify credentials -- test the connection with a signed request.

- Sync balances -- pull your current holdings from Binance.

- Place orders -- execute spot market orders (BUY with quoteOrderQty, SELL with quantity).

- Fetch market data -- download candle history via the Binance REST API.

Botmarley automatically applies LOT_SIZE and MARKET_LOT_SIZE filters from Binance exchangeInfo to ensure order quantities are valid.

A Binance account operates with real money. Double-check your strategy in Paper mode before pointing it at a Binance account.

Verification States

Every account has a verification status that reflects whether Botmarley has successfully tested the connection to the exchange.

| Status | Badge Color | Meaning |

|---|---|---|

| Unverified | Yellow | Credentials have been entered but not yet tested. |

| Verified | Green | Botmarley connected to the exchange and confirmed the credentials work. |

| Failed | Red | The last verification attempt failed (bad key, wrong permissions, network error). |

| N/A | Gray | Verification does not apply to this account type (Paper accounts). |

Verification is performed by making a signed API request to the exchange's private balance endpoint. If the exchange responds without errors, the credentials are marked Verified. If the exchange returns an authentication error or the request fails, the status is set to Failed.

If verification fails, check that your API key has not expired and that you copied both the key and the secret correctly. Kraken secrets are base64-encoded strings -- make sure you copied the entire value without extra whitespace.

When to Use Paper vs. Real Accounts

flowchart TD

A["New strategy idea"] --> B{"Tested in backtesting?"}

B -- No --> C["Run backtest with Paper account"]

C --> B

B -- Yes --> D{"Happy with results?"}

D -- No --> E["Adjust strategy parameters"]

E --> C

D -- Yes --> F{"Ready for real money?"}

F -- No --> G["Run live Paper session\n(simulated orders)"]

G --> F

F -- Yes --> H["Switch to Kraken account\nfor live trading"]

The recommended workflow:

- Backtest first -- use a Paper account and historical data to validate your strategy logic.

- Paper-trade live -- run the strategy in live mode against a Paper account. This exercises the real-time data feed without risking funds.

- Go live -- once confident, create or select a verified Kraken account and start a live trading session.

This progression lets you catch problems early, before any real capital is at stake.

Managing Accounts

This chapter walks through every account management operation: creating, verifying, syncing, editing, and deleting accounts. All of these actions are performed from the Accounts page at /accounts.

Creating a New Account

The Accounts page lists all your configured accounts with their type, verification status, and available actions.

- Navigate to the Accounts page using the sidebar or by visiting

/accounts. - Click the Add Account button in the top-right corner. A modal dialog opens.

- Fill in the form fields:

| Field | Required | Description |

|---|---|---|

| Name | Yes | A label for the account (e.g. "Kraken Main", "Paper Test"). |

| Description | No | Optional notes for your own reference. |

| Account Type | Yes | Choose Paper, Kraken, or Binance from the dropdown. |

| API Key | Kraken/Binance only | Your exchange API key. Hidden when Paper is selected. |

| API Secret | Kraken/Binance only | Your exchange API secret. Hidden when Paper is selected. |

- Click Create.

Botmarley redirects you back to the accounts list. Your new account appears in the table with a verification status of Unverified (for exchange accounts) or N/A (for Paper accounts).

For Paper accounts, you can skip the API fields entirely. Just give it a name, select "Paper (Simulated)", and click Create.

Getting Exchange API Keys

To connect an exchange account, you need an API key pair generated from the exchange's website.

Kraken API Keys

- Log in to your Kraken account at https://www.kraken.com.

- Navigate to Settings (gear icon) then API.

- Click Create API Key (or Generate New Key).

- Give the key a descriptive name (e.g. "Botmarley Trading Bot").

- Set the permissions (see below).

- Click Generate Key.

- Copy both the API Key and the Private Key (secret) immediately. Kraken only shows the secret once. If you lose it, you must generate a new key pair.

- Paste the key and secret into Botmarley's account creation form.

Kraken displays the API secret (Private Key) only at the moment of creation. There is no way to retrieve it later. If you navigate away before copying it, you will need to delete the key and generate a new one.

Binance API Keys

- Log in to your Binance account at https://www.binance.com.

- Navigate to Account then API Management.

- Click Create API and give the key a label (e.g. "Botmarley Trading Bot").

- Complete any required security verification (2FA).

- Copy both the API Key and the Secret Key immediately. Binance only shows the secret at creation time.

- Paste the key and secret into Botmarley's account creation form.

Binance displays the API Secret Key only at the moment of creation. If you close the dialog before copying it, you will need to delete the key and generate a new one.

Setting API Key Permissions

Both Kraken and Binance let you control what each API key can do. The permissions you need depend on how you plan to use Botmarley.

Kraken Permissions

Read-only (monitoring and portfolio tracking)

If you only want to sync balances and track your portfolio, enable:

- Query Funds -- allows Botmarley to read your account balances.

- Query Open Orders & Trades -- allows Botmarley to read trade history.

This is the safest option. The key cannot place or cancel orders.

Trading (live bot execution)

If you want Botmarley to place orders on your behalf during live trading sessions, you also need:

- Create & Modify Orders -- allows Botmarley to submit new orders.

- Cancel/Close Orders -- allows Botmarley to cancel open orders.

Permissions to avoid

Unless you have a specific reason, do not enable:

- Withdraw Funds -- Botmarley never needs withdrawal access.

- Access WebSockets API -- not currently required for Botmarley's Kraken integration (REST is used).

Binance Permissions

Read-only (monitoring and portfolio tracking)

- Enable Reading -- allows Botmarley to read your account balances and trade history.

Trading (live bot execution)

- Enable Spot & Margin Trading -- allows Botmarley to place spot market orders.

Permissions to avoid

- Enable Withdrawals -- Botmarley never needs withdrawal access.

- Enable Futures -- Botmarley currently supports spot trading only.

Only grant the permissions Botmarley actually needs. Never enable withdrawal permissions for a bot API key. If a key is ever compromised, withdrawal access would put your funds at direct risk.

Verifying Credentials

After creating an exchange account, its status is Unverified. Verification confirms that the API key and secret are correct and that Botmarley can reach the exchange.

How to verify

- On the Accounts page, find the account row in the table.

- Click the Verify button (checkmark icon or "Verify" label).

- Botmarley enqueues an

AccountVerifytask and redirects you to the Tasks page. - The task worker picks up the job and makes a signed request to the exchange's balance endpoint. Kraken uses HMAC-SHA512 signing against

/0/private/Balance; Binance uses HMAC-SHA256 signing against/api/v3/account. - If the exchange responds successfully, the account status changes to Verified.

- If authentication fails, the status changes to Failed.

You can check the result by returning to the Accounts page or watching the task complete on the Tasks page.

Verification is a one-time check. If you later rotate your API keys on the exchange, you will need to update the credentials in Botmarley and re-verify.

Troubleshooting verification failures

| Symptom | Likely cause | Fix |

|---|---|---|

| Status stays "Failed" | Incorrect API key or secret | Double-check the values; re-paste from the exchange if needed. |

| Status stays "Failed" | API key expired or revoked | Generate a new key on the exchange. |

| Status stays "Failed" | Missing read/query permissions | Edit the key on the exchange and enable the required permission. |

| Task never completes | Network issue or server not running | Check the server logs and internet connectivity. |

Syncing Account Assets

Syncing pulls the current token balances from the exchange into Botmarley's database. This is how Botmarley knows what you hold.

How to sync

- On the Accounts page, click the Sync button on the account row.

- Botmarley enqueues an

AccountSynctask. - The task worker calls the exchange API (Kraken's

/0/private/Balanceor Binance's/api/v3/account), retrieves all non-zero balances, normalizes the token names, and upserts them into theaccount_assetstable. - Once complete, the account's asset list is updated.

You can expand an account row to see its assets, or visit the Portfolio page for an aggregated view across all accounts.

Paper accounts cannot be synced from an exchange (there is no exchange). Their balances are set manually or updated by the trading engine during simulated sessions.

Token name normalization

Kraken uses internal token names that differ from standard symbols. Botmarley normalizes them automatically during sync:

| Kraken name | Normalized |

|---|---|

| XXBT | XBT |

| XETH | ETH |

| ZUSD | USD |

| XLTC | LTC |

| XXRP | XRP |

Tokens that do not match a known pattern (e.g. DOT, USDC) are stored as-is.

Binance uses standard token symbols (BTC, ETH, USDC, etc.), so no normalization is needed for Binance accounts.

Editing an Account

- On the Accounts page, click the Edit button (pencil icon) on the account row.

- The edit modal opens with the current name, description, and type pre-filled.

- Modify the fields you want to change.

- For credentials: leave the API Key and API Secret fields empty to keep the existing values. Only fill them in if you want to replace them.

- Click Save Changes.

After editing credentials, you should re-verify the account to confirm the new keys work.

Deleting an Account

- On the Accounts page, click the Delete button on the account row.

- Botmarley deletes the account and all associated assets from the database.

Deleting an account removes it and all its stored asset data from Botmarley's database. This cannot be undone. Your funds on the actual exchange are not affected -- only Botmarley's local record is removed.

Deletion also cascades to portfolio snapshots associated with that account. Aggregate (cross-account) portfolio snapshots are not deleted, but they will no longer include the removed account in future syncs.

API Key Security

Botmarley stores API credentials in the local PostgreSQL database. Here are the safeguards in place and the precautions you should take.

What Botmarley does

- Secrets are never sent to the browser. The

Accountstruct has ato_view()method that masks the API key (showing only the first and last 4 characters) and omits the secret entirely. - Credentials stay local. Botmarley is a single-tenant application running on your machine. There is no cloud service, no third-party server, and no telemetry that transmits your keys.

What you should do

- Never share your API secret with anyone.

- Never enable Withdraw permissions on keys used by bots.

- Use a dedicated API key for Botmarley rather than reusing one from another tool.

- Rotate keys periodically -- delete the old key on the exchange and generate a new one.

- Restrict IP access if the exchange supports it for your key -- lock the key to the IP address where Botmarley runs.

- Back up your database carefully -- the PostgreSQL database contains the raw API secret. Treat database dumps with the same care as the secrets themselves.

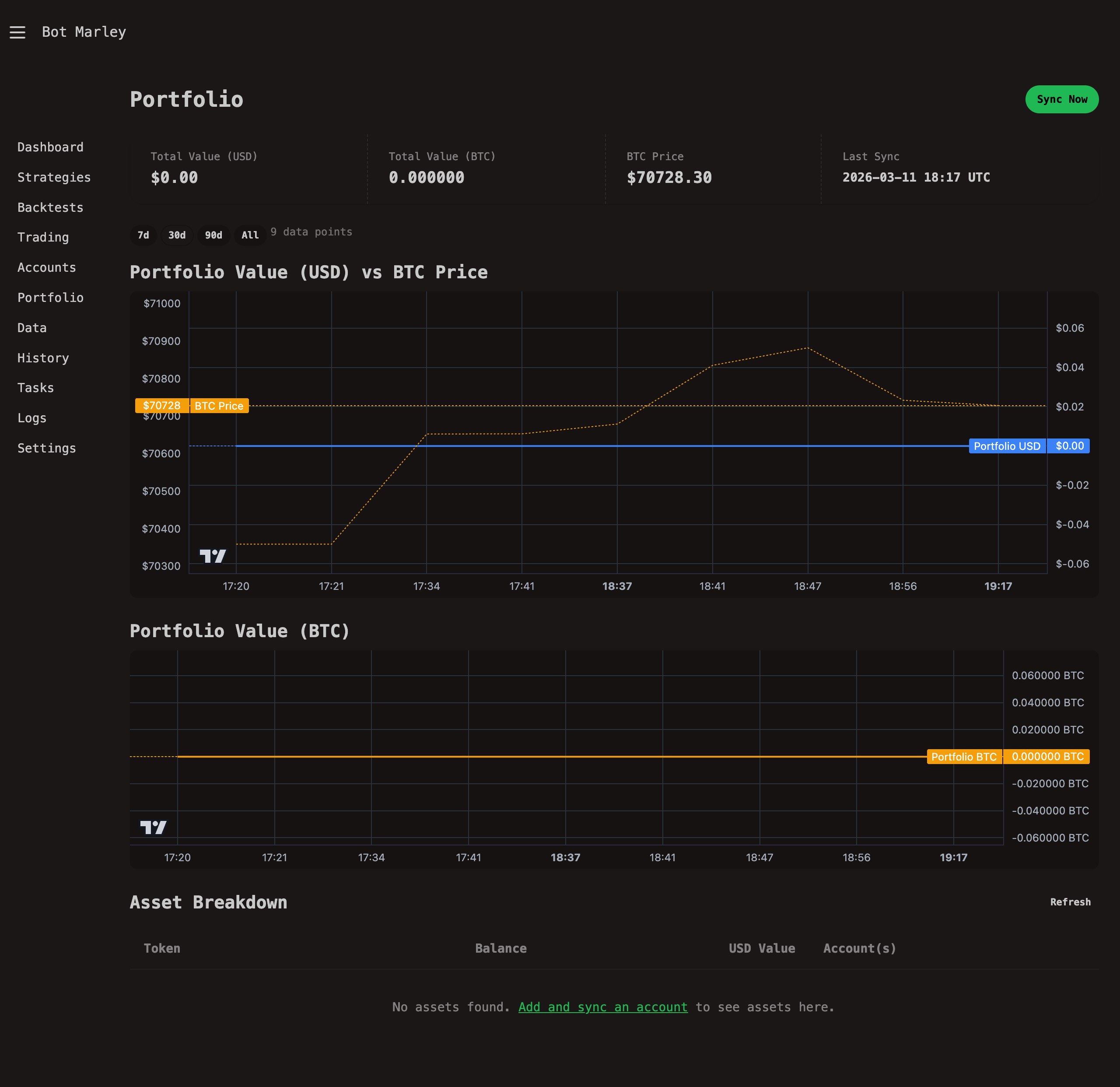

Portfolio Tracking

The Portfolio page gives you a consolidated view of everything you hold across all your accounts -- Paper and exchange alike -- valued in both USD and BTC, updated automatically over time.

What Is Portfolio Tracking?

Portfolio tracking answers a simple question: how much is everything worth, right now and over time?

Botmarley periodically takes a "snapshot" of your portfolio. Each snapshot records:

- The total value in USD across all accounts.

- The total value in BTC (your USD total divided by the current BTC price).

- The BTC/USD price at that moment.

- A per-token breakdown showing balance and USD value for each asset.

By storing snapshots over time, Botmarley can draw charts showing how your portfolio value has changed -- and whether you are gaining or losing ground relative to Bitcoin itself.

How It Works

Portfolio syncing follows a pipeline that runs on a fixed schedule and can also be triggered manually.

Automatic sync schedule

A background scheduler starts when the Botmarley server boots. After an initial 60-second startup delay, it enqueues a PortfolioSync task every 1 hour. The task worker picks it up and runs the full sync pipeline.

The sync pipeline

flowchart LR

A["Scheduler\n(every 1h)"] -->|enqueues task| B["Task Worker"]

B --> C["Sync Exchange\nAccounts"]

C --> D["Query All\nAccount Assets"]

D --> E["Fetch USD Prices\n(Kraken Ticker API)"]

E --> F["Compute Totals\n(USD + BTC)"]

F --> G["Store Snapshot\n(PostgreSQL)"]

In detail, each sync performs these steps:

- Sync verified exchange accounts -- for every exchange account with status "Verified", Botmarley calls the exchange API to pull the latest balances. Failed syncs for individual accounts are logged but do not stop the pipeline.

- Query all account assets -- reads every non-zero asset balance across all accounts (including Paper) from the database.

- Fetch USD prices -- calls the Kraken public Ticker API to get current USD prices for each unique token. Stablecoins and fiat are handled locally (see below).

- Compute totals -- sums up

balance * pricefor every asset to gettotal_value_usd. Fetches the BTC/USD price separately and calculatestotal_value_btc = total_value_usd / btc_price. - Store snapshot -- inserts one aggregate row (with

account_id = NULL) into theportfolio_snapshotstable, including a JSON breakdown of per-token values.

The Portfolio Page

The portfolio page is located at /portfolio. It has several sections, described from top to bottom.

Summary Cards

Four stat cards appear at the top of the page:

| Card | Description | Example |

|---|---|---|

| Total Value (USD) | Sum of all assets across all accounts, converted to USD. | $12,345.67 |

| Total Value (BTC) | Your USD total divided by the current BTC price. | 0.142857 |

| BTC Price | The latest BTC/USD price fetched from Kraken. | $86,420.00 |

| Last Sync | Timestamp of the most recent portfolio snapshot. | 2026-03-11 14:00 UTC |

If no snapshots exist yet (fresh install), the page shows an empty state with buttons to manage accounts or run a first sync.

Range Selector

Below the summary cards, a row of small buttons lets you control the time range for the charts:

| Button | Time range |

|---|---|

| 7d | Last 7 days |

| 30d | Last 30 days (default) |

| 90d | Last 90 days |

| All | All available history |

Switching ranges fetches new data from /api/portfolio/chart?range=... and updates both charts without a full page reload. A small label next to the buttons shows how many data points are in the current view.

USD Chart: Portfolio Value + BTC Price Overlay

The first chart displays two lines on a dual-axis layout:

- Portfolio USD (blue, right axis) -- your total portfolio value over time in US dollars.

- BTC Price (amber/dashed, left axis) -- the Bitcoin price over the same period.

This overlay lets you visually compare whether your portfolio is outperforming or underperforming a simple Bitcoin hold. The charts are rendered using Lightweight Charts loaded from a CDN.

BTC Chart: Portfolio Value in BTC

The second chart shows a single amber line: your portfolio's value expressed in Bitcoin. If this line trends upward, you are accumulating more BTC-equivalent value over time, even if the USD value moves sideways.

Asset Breakdown Table

Below the charts, a table lists every token you hold across all accounts:

| Column | Description |

|---|---|

| Token | The asset symbol (BTC, ETH, USDC, etc.) |

| Balance | Total holdings of that token across all accounts. |

| USD Value | Balance multiplied by the current USD price. |

| Account(s) | Which accounts hold this token and how much each one holds. |

The table includes a Refresh button that fetches the latest data via HTMX without reloading the page. Assets are sorted by USD value in descending order, so your largest holdings appear first.

Manual Sync

You do not have to wait for the hourly scheduler. To trigger a portfolio sync on demand:

- Go to the Portfolio page (

/portfolio). - Click the Sync Now button in the top-right corner.

- Botmarley enqueues a

PortfolioSynctask and redirects you back to the portfolio page. - The task worker processes the sync (usually completes within a few seconds).

- Refresh the page to see updated values and charts.

After adding a new exchange account and verifying it, click "Sync Now" on the Portfolio page to immediately pull in its balances rather than waiting for the next scheduled sync.

How Prices Are Fetched

Botmarley uses the Kraken public Ticker API to fetch USD prices. This endpoint requires no authentication and has generous rate limits.

The API call

A single request is made to https://api.kraken.com/0/public/Ticker?pair=XXBTZUSD,XETHZUSD,... with all needed trading pairs joined by commas. The response includes the last trade price for each pair, which Botmarley uses as the current price.

Token-to-pair mapping

Botmarley maps normalized token names to Kraken trading pair identifiers:

| Token | Kraken Pair |

|---|---|

| BTC / XBT | XXBTZUSD |

| ETH | XETHZUSD |

| LTC | XLTCZUSD |

| XRP | XXRPZUSD |

| XLM | XXLMZUSD |

| (others) | {TOKEN}USD |

For tokens that Kraken does not list, the price falls back to 0.0 and a warning is logged.

Stablecoin Handling

Stablecoins and fiat currencies are handled without an API call:

| Tokens | Assumed USD price |

|---|---|

| USD, USDC, USDT, BUSD, DAI, TUSD, USDP, GUSD | $1.00 |

| EUR, GBP, CAD, AUD, CHF, JPY | ~$1.00 (rough approximation) |

The fiat approximation (treating EUR, GBP, etc. as $1.00) is a simplification. For portfolios with significant fiat holdings in non-USD currencies, the total USD value will be approximate. A more accurate forex conversion may be added in a future release.

Architecture: Full Sync Flow

The following diagram shows the complete lifecycle of a portfolio sync, from trigger through to the stored snapshot.

sequenceDiagram

participant S as Scheduler (1h) /<br>Manual Button

participant Q as Task Queue

participant W as Task Worker

participant K as Kraken API

participant DB as PostgreSQL

S->>Q: Enqueue PortfolioSync task

Q->>W: Dequeue task

Note over W: Step 1: Sync exchange accounts

W->>DB: List verified exchange accounts

DB-->>W: [Kraken accounts]

loop Each verified account

W->>K: POST /0/private/Balance (signed)

K-->>W: Token balances

W->>DB: Upsert account_assets

end

Note over W: Step 2: Gather all assets

W->>DB: SELECT token, balance FROM account_assets

DB-->>W: All non-zero balances

Note over W: Step 3: Fetch prices

W->>K: GET /0/public/Ticker?pair=...

K-->>W: USD prices per pair

Note over W: Step 4-5: Compute and store

W->>W: total_usd = SUM(balance * price)<br>total_btc = total_usd / btc_price

W->>DB: INSERT INTO portfolio_snapshots

DB-->>W: Snapshot ID

W->>Q: Mark task complete

If a single exchange account fails to sync (e.g., temporary network error), the pipeline continues with the remaining accounts. The snapshot will still be created using whatever data was successfully retrieved. Check the Activity Logs or Task Queue for details on any failures.

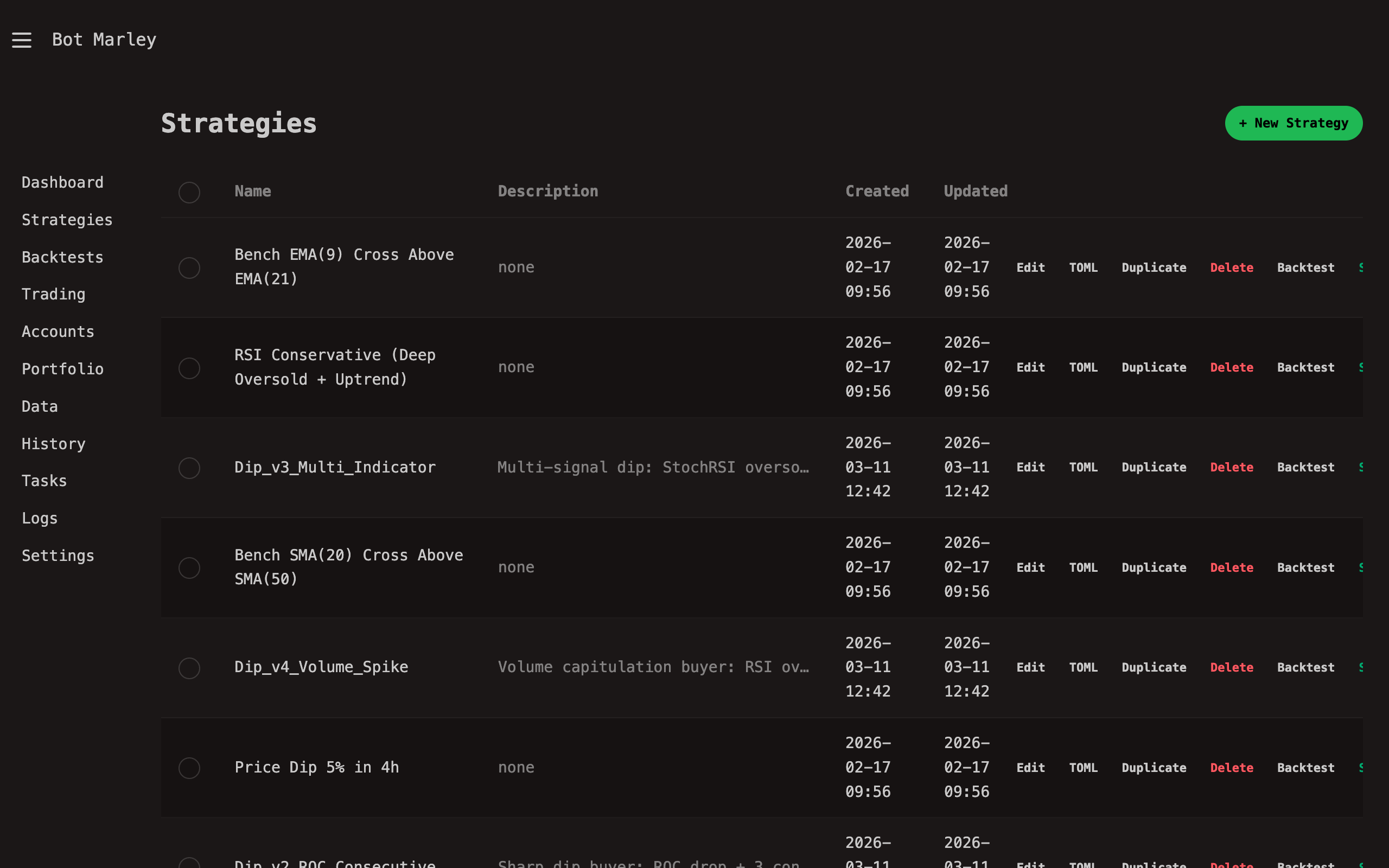

Strategies Overview

What Is a Trading Strategy?

A trading strategy is a set of rules that tell Botmarley when to buy and when to sell a cryptocurrency. Instead of watching charts all day and making emotional decisions, you define your rules once, and Botmarley follows them automatically -- 24 hours a day, 7 days a week.

Think of a strategy as a recipe:

- Ingredients are market data (prices, indicators, candle patterns).

- Instructions are the rules (if RSI drops below 30, buy).

- The result is consistent, disciplined trading without human emotion.

The Strategies List

The web interface provides a central place to manage all your strategies. From the list page you can edit, duplicate, delete, backtest, or start live trading for any strategy with a single click.

How Botmarley Strategies Work

Botmarley strategies are defined as TOML files -- simple, human-readable text files that describe a rule engine. Each strategy file lives in the strats/ directory and contains:

- Metadata -- the strategy's name, description, and position limits.

- Actions -- a list of things the bot can do (open a position, add to it, or sell).

- Triggers -- conditions that must be true for each action to fire.

Botmarley's strategy engine is exchange-agnostic. The same strategy TOML file works for any trading pair -- you select the pair when you start a backtest or live session, not in the strategy itself.

Strategy Evaluation Flow

Every time a new candle closes, Botmarley evaluates your strategy. Here is how the evaluation loop works:

flowchart TD

A["New Candle Received"] --> B["For Each Action in Strategy"]

B --> C{"Check ALL Triggers<br/>(AND logic)"}

C -- "All triggers TRUE" --> D["Execute Action<br/>(open_long / buy / sell)"]

C -- "Any trigger FALSE" --> E["Skip This Action"]

D --> F["Update Position State"]

E --> F

F --> G{"More Actions?"}

G -- "Yes" --> B

G -- "No" --> H["Wait for Next Candle"]

H --> A

style A fill:#4a9eff,color:#fff

style D fill:#22c55e,color:#fff

style E fill:#6b7280,color:#fff

style H fill:#4a9eff,color:#fff

Key points about evaluation:

- Each action is evaluated independently -- one strategy can have multiple buy and sell actions, and each is checked every tick.

- Triggers within an action are AND-combined -- ALL triggers must be true for the action to fire.

- Actions are evaluated in order -- from first to last as written in the TOML file.

Basic Strategy Anatomy

A Botmarley strategy TOML file has two main sections:

1. The [meta] Section

This defines your strategy's identity and global settings:

[meta]

name = "My First Strategy"

description = "A simple RSI-based entry and exit"

max_open_positions = 3

| Field | Required | Description |

|---|---|---|

name | Yes | Human-readable name for the strategy |

description | No | Optional explanation of the strategy's logic |

max_open_positions | No | Maximum concurrent open positions. Omit for unlimited. |

2. The [[actions]] Array

Each [[actions]] block defines one thing the bot can do, along with the conditions that must be met:

[[actions]]

type = "open_long" # What to do: open_long, buy, or sell

amount = "100 USDC" # How much: fixed amount or percentage

average_price = false # Whether to average the entry price (DCA)

[[actions.triggers]] # When to do it: one or more trigger conditions

indicator = "rsi_14"

operator = "<"

target = "30"

A Simple Complete Example

Here is a complete, working strategy that buys when RSI is oversold and sells when it recovers:

[meta]

name = "RSI_Scalper"

# ACTION 1: Open a position when RSI drops below 30

[[actions]]

type = "open_long"

amount = "100 USDC"

[[actions.triggers]]

indicator = "rsi_14"

operator = "<"

target = "30"

# ACTION 2: Sell half when RSI recovers to 50

[[actions]]

type = "sell"

amount = "50%"

[[actions.triggers]]

indicator = "rsi_14"

operator = ">"

target = "50"

# ACTION 3: Sell everything when RSI reaches 70

[[actions]]

type = "sell"

amount = "100%"

[[actions.triggers]]

indicator = "rsi_14"

operator = ">"

target = "70"

What this strategy does, step by step:

- Action 1 watches RSI(14). When it drops below 30 (oversold territory), the bot opens a new position by buying 100 USDC worth of the asset.

- Action 2 watches for RSI to rise above 50. When it does, the bot sells 50% of the position to lock in partial profit.

- Action 3 watches for RSI to rise above 70 (overbought territory). When it does, the bot sells the remaining 100% of the position to fully exit.

Start simple. A strategy with 2-3 actions is often more effective than a complex one with 10 actions. You can always add complexity after backtesting confirms the base logic works.

What's Next?

Now that you understand how strategies are structured, explore the following topics:

- Strategy Editor -- how to create and edit strategies in the web interface.

- Actions -- detailed explanation of

open_long,buy, andsell. - Indicators Reference -- every indicator Botmarley supports.

- Timeframes -- how multi-timeframe analysis works.

- Position Management -- DCA, position limits, and partial sells.

- Strategy Examples -- complete, battle-tested strategies you can use as starting points.

Strategy Editor

The Strategy Editor is where you create, edit, and manage your trading strategies. Access it from the sidebar by clicking Strategies or navigating directly to /strats.

The Strategies List Page

The strategies list page (/strats) shows all your saved strategies. For each strategy you can see:

- The strategy name and description

- When it was created and last updated

- Action buttons for editing, duplicating, backtesting, and deleting

flowchart LR

A["Strategies List<br/>/strats"] --> B["Edit<br/>/strats/edit/{id}"]

A --> C["New Strategy<br/>/strats/new"]

A --> D["Duplicate"]

A --> E["Delete"]

A --> F["Backtest"]

B --> G["Save"]

C --> G

G --> A

style A fill:#4a9eff,color:#fff

style G fill:#22c55e,color:#fff

Creating a New Strategy

To create a new strategy:

- Navigate to

/strats(click Strategies in the sidebar). - Click the New Strategy button.

- The editor opens with an empty TOML document.

- Write your strategy in TOML format (see Strategy Overview for the structure).

- Click Save.

The editor assigns a unique ID (UUID) to your new strategy automatically.

If you are new to writing strategies, start by duplicating one of the existing strategies and modifying it. This is faster than writing from scratch and helps you learn the TOML structure by example.

The Visual Strategy Editor

The visual editor provides a form-based interface for building strategies without writing TOML by hand. You can add actions, configure triggers, set indicator parameters, and define position management rules -- all through a structured UI.

The TOML Text Editor

The strategy editor at /strats/edit/{id} provides a text-based TOML editor where you write your strategy directly. The editor shows the raw TOML content of your strategy file.

A typical editing session looks like this:

- The

[meta]section is at the top -- set your strategy's name and description here. - Below that, define your

[[actions]]blocks with their triggers. - As you type, the editor validates your TOML in real time.

Editor Layout

The editor page provides:

- Strategy name displayed at the top

- TOML text area for editing the strategy content

- Save button to persist changes

- Back to list link to return to

/strats

Real-Time Validation

Every time you save or validate your strategy, Botmarley checks the TOML content for errors. The validation endpoint (POST /api/strats/validate) checks:

- TOML syntax -- is the file valid TOML?

- Required fields -- does

[meta]have aname? Does each action have atypeandamount? - Valid action types -- only

open_long,buy, andsellare accepted. - Amount format -- must be

"100 USDC"(fixed) or"50%"(percentage). - Indicator format -- must match known patterns like

rsi_14,sma_50,bb_lower. - Operator validity -- must be one of

>,<,=,cross_above,cross_below. - Timeframe validity -- if specified, must be

1m,5m,15m,1h,4h, or1d. - Period ranges -- indicator periods must be between 1 and 200.

max_open_positions-- if set, must be 1 or greater.

When validation fails, the error response includes:

| Field | Description |

|---|---|

field_path | Where the error is, e.g. actions[0].triggers[1].operator |

error_code | Machine-readable code like INVALID_FORMAT or REQUIRED |

message | Human-readable description of the problem |

suggestion | Hint for how to fix the error |

Botmarley will not let you save an invalid strategy. Fix all validation errors before saving. This prevents broken strategies from being used in backtests or live trading.

Common Validation Errors

| Error | Cause | Fix |

|---|---|---|

INVALID_ACTION_TYPE | Typo in action type | Use open_long, buy, or sell |

INVALID_AMOUNT_FORMAT | Missing unit or wrong format | Use "100 USDC" or "50%" |

INVALID_PERIOD | Non-numeric indicator period | Use rsi_14 not rsi_fourteen |

INVALID_PERIOD_RANGE | Period 0 or > 200 | Keep periods between 1 and 200 |

REQUIRED | Missing indicator or operator | Add the missing field to your trigger |

INVALID_TIMEFRAME | Unknown timeframe string | Use 1m, 5m, 15m, 1h, 4h, or 1d |

INVALID_OPERATOR | Unknown comparison operator | Use >, <, =, cross_above, cross_below |

Saving Strategies

When you click Save, Botmarley:

- Validates the TOML content server-side.

- If valid, writes the TOML file to the

strats/directory with the strategy's UUID as the filename. - Returns a success response with the strategy ID.

- Logs the save action to the activity log.

If the strategy is new (no ID yet), a new UUID is generated. If you are editing an existing strategy, the same ID is reused and the file is overwritten.

Strategy files are stored as plain .toml files in the strats/ directory. The filename is the UUID (e.g., 6f814a05-73e8-483f-8963-aa8a4ab8e1e7.toml). You can also edit these files directly with any text editor -- Botmarley reads them from disk.

Duplicating Strategies

To duplicate a strategy:

- Go to the strategies list (

/strats). - Click the Duplicate button on the strategy you want to copy.

- Botmarley creates a copy with " (Copy)" appended to the name.

- You are redirected to the editor for the new copy.

This is useful when you want to create variations of an existing strategy (for example, testing different RSI thresholds or DCA levels).

Deleting Strategies

To delete a strategy:

- Go to the strategies list (

/strats). - Click the Delete button on the strategy you want to remove.

- The TOML file is removed from the

strats/directory. - You are redirected back to the list.

Deleting a strategy is permanent. The TOML file is removed from disk. If you think you might want the strategy later, duplicate it first or keep a backup.

Bulk Delete

You can also select multiple strategies and delete them all at once using the bulk delete feature on the strategies list page. Select the checkboxes next to the strategies you want to remove, then click the bulk delete button.

Discovering Available Pairs

When you open the backtest modal from the strategies list page, Botmarley automatically scans your downloaded market data to show you which trading pairs are available. This is based on the .arrow files in your data storage directory.

The available pairs and their date ranges are shown in the backtest form, so you can select:

- Which pair to backtest against (e.g.,

XBTUSD,ETHUSD) - Start and end dates -- pre-filled based on your actual data range

If you do not see the pair you want, you need to download its historical data first. Go to the Market Data section to download candle history from Kraken.

Actions

Actions are the building blocks of your strategy. Each action defines what the bot should do when its trigger conditions are met. A strategy can have any number of actions, and each is evaluated independently on every candle.

The Three Action Types

Botmarley supports three action types, each serving a distinct purpose in the lifecycle of a trade:

flowchart LR

A["open_long<br/>Open new position"] --> B["buy<br/>Add to position (DCA)"]

B --> C["sell<br/>Exit position"]

style A fill:#22c55e,color:#fff

style B fill:#4a9eff,color:#fff

style C fill:#ef4444,color:#fff

open_long -- Open a New Position

The open_long action creates a new position by buying an asset. This is the entry point of any trade.

When to use: Use open_long for the initial entry into a trade. This action only fires when there is no existing open position (or when max_open_positions has not been reached).

Example:

[[actions]]

type = "open_long"

amount = "100 USDC"

average_price = false

[[actions.triggers]]

indicator = "rsi_14"

operator = "<"

target = "30"

This opens a new position worth 100 USDC when RSI(14) drops below 30.

open_long is the only action type that creates a new position. If you already have an open position and want to add more, use buy instead.

buy -- Add to an Existing Position (DCA)

The buy action adds to an already open position. This is how you implement Dollar-Cost Averaging (DCA) -- buying more when the price drops to lower your average entry price.

When to use: Use buy to add to a position that was opened by open_long. This action only fires when a position is already open.

Example:

[[actions]]

type = "buy"

amount = "200 USDC"

average_price = true

[[actions.triggers]]

type = "pos_price_change"

value = "-2%"

max_count = 1

This adds 200 USDC to the existing position when the price drops 2% from the entry price. The average_price = true flag means the entry price is recalculated (see average_price explained below). The max_count = 1 ensures this DCA level only triggers once per position.

sell -- Exit a Position

The sell action exits part or all of an open position. You can sell a percentage of your position or sell everything.

When to use: Use sell for taking profit, cutting losses (stop-loss), or any exit condition.

Example -- partial exit:

[[actions]]

type = "sell"

amount = "50%"

[[actions.triggers]]

indicator = "rsi_14"

operator = ">"

target = "50"

This sells half the position when RSI rises above 50, locking in partial profit while letting the rest ride.

Example -- full exit:

[[actions]]

type = "sell"

amount = "100%"

[[actions.triggers]]

type = "pos_price_change"

value = "3%"

This sells the entire position when the price rises 3% from entry, closing the trade completely.

Amount Formats

Every action requires an amount field that specifies how much to buy or sell. Botmarley supports two formats:

Fixed Amount: "100 USDC"

A fixed dollar amount. The bot buys or sells exactly this much.

amount = "100 USDC"

When to use: For entries and DCA levels where you want predictable position sizing. Most strategies use fixed amounts for open_long and buy actions.

Supported currencies: USDC, USD, BTC, ETH, and other standard ticker symbols.

Percentage Amount: "50%"

A percentage of either the available balance (for buys) or the current position size (for sells).

amount = "50%" # Sell half the position

amount = "100%" # Sell the entire position

When to use:

- For sell actions:

"50%"means sell half your position;"100%"means exit completely. - For buy actions:

"50%"means use 50% of available balance.

Use percentage amounts for sells and fixed amounts for buys. This gives you predictable entry sizing while allowing flexible exit sizing. For example, selling "50%" first and then "100%" of the remainder lets you scale out of a position as the price rises.

Amount Format Rules

| Format | Example | Valid For | Description |

|---|---|---|---|

| Fixed | "100 USDC" | open_long, buy | Buy exactly 100 USDC worth |

| Fixed | "0.01 BTC" | open_long, buy | Buy exactly 0.01 BTC |

| Percentage | "50%" | buy, sell | 50% of balance or position |

| Percentage | "100%" | sell | Sell the entire position |

Negative amounts are not allowed. The amount must be a positive number. Use the action type (sell) to indicate selling, not a negative amount.

average_price Explained

The average_price flag controls whether the bot recalculates the position's entry price after a buy or open_long action. This is the core mechanism behind Dollar-Cost Averaging (DCA).

How It Works

When average_price = true and the bot buys more of an asset, the entry price is recalculated as a weighted average:

new_entry_price = (old_qty * old_price + new_qty * new_price) / (old_qty + new_qty)

Example:

- You open a position: buy 100 USDC worth of BTC at $50,000. Entry price = $50,000.

- Price drops to $48,000. A DCA

buytriggers: buy 200 USDC more at $48,000. - With

average_price = true, the new entry price becomes:- Total cost: $100 + $200 = $300

- Total BTC: 0.002 + 0.004167 = 0.006167 BTC

- New entry price: $300 / 0.006167 = $48,649

- Now the price only needs to rise to $48,649 (not $50,000) to break even.

When to Use It

| Scenario | average_price | Why |

|---|---|---|

| DCA buy on dip | true | Lower your average entry so you break even sooner |

| Adding to a winner | false | Keep the original entry price for P&L tracking |

Initial open_long | false | No previous position to average with |

All sell actions | false | Selling does not affect entry price |

The average_price flag is only meaningful for open_long and buy actions. Setting it on a sell action has no effect.

Multiple Actions: How They Work Together

A strategy typically has multiple actions -- at least one entry (open_long) and one exit (sell). Here is how they interact:

Evaluation Order

Actions are evaluated independently and in order on every candle:

flowchart TD

A["Candle Closes"] --> B["Evaluate Action 1<br/>(open_long)"]

B --> C["Evaluate Action 2<br/>(buy / DCA level 1)"]

C --> D["Evaluate Action 3<br/>(buy / DCA level 2)"]

D --> E["Evaluate Action 4<br/>(sell / take profit)"]

E --> F["Evaluate Action 5<br/>(sell / stop loss)"]

style A fill:#4a9eff,color:#fff

Key Rules

open_longonly fires when no position is open (or whenmax_open_positionsallows another).buyonly fires when a position IS open -- it has nothing to add to otherwise.sellonly fires when a position IS open -- you cannot sell what you do not have.- Multiple sell actions can coexist -- you might have a take-profit sell at +3% AND a stop-loss sell at -8%. Whichever condition is met first will fire.

- After a 100% sell, the position is closed -- subsequent

buytriggers will not fire untilopen_longcreates a new position.

Typical Action Structure

Most strategies follow this pattern:

# 1. Entry

[[actions]]

type = "open_long"

amount = "100 USDC"

# ... entry triggers ...

# 2. DCA Level 1 (optional)

[[actions]]

type = "buy"

amount = "200 USDC"

average_price = true

# ... dip trigger ...

# 3. DCA Level 2 (optional)

[[actions]]

type = "buy"

amount = "300 USDC"

average_price = true

# ... deeper dip trigger ...

# 4. Take Profit

[[actions]]

type = "sell"

amount = "100%"

# ... profit trigger ...

# 5. Stop Loss

[[actions]]

type = "sell"

amount = "100%"

# ... loss trigger ...

You can have multiple sell actions with different conditions. For example, sell 50% at +2% profit and the remaining 100% at +5% profit. This lets you scale out of a position gradually.

Triggers Overview

Triggers are the decision engine of every Botmarley strategy. An action (buy, sell, open position) only executes when its triggers say "go." Without triggers, an action would never fire. Without the right triggers, your strategy would trade at the wrong time.

Think of it this way:

- An action answers what to do (buy 100 USDC, sell 50%, open a long position).

- A trigger answers when to do it (RSI dropped below 30, price fell 3% from entry, the 4h candle just closed).

Every action has one or more triggers attached to it. When all of them are satisfied at the same moment, the action fires.

The Three Trigger Types

Botmarley supports three categories of triggers. Each watches a different kind of market signal:

| Type | What It Watches | Example |

|---|---|---|

| Technical | Indicator values and crossovers | RSI(14) drops below 30, SMA(50) crosses above SMA(200) |

| PriceChange | Price movement, position P&L, time, momentum | Price dropped 3% in the last hour, position is up 2% from entry |

| NextCandle | Candle close events | The 4h candle just closed, the daily candle just closed |

You will often combine these types on the same action. For example, "buy when the 4h candle closes AND RSI is below 35" uses a NextCandle trigger together with a Technical trigger.

The dedicated chapters cover each type in depth:

- Technical Indicators -- indicator comparisons and crossovers

- Price Change -- price movement, P&L tracking, trailing stops, time exits

- Next Candle -- scheduled candle-close events

AND Logic: Multiple Triggers on One Action

When you attach multiple triggers to a single action, Botmarley treats them as AND conditions. Every trigger must be true simultaneously for the action to fire.

graph LR

T1["Trigger 1<br/>RSI(14) < 30"]

T2["Trigger 2<br/>SMA(50) > SMA(200)"]

T3["Trigger 3<br/>Price fell -3%"]

AND{{"ALL must<br/>be true"}}

A["Action fires:<br/>Buy 100 USDC"]

T1 --> AND

T2 --> AND

T3 --> AND

AND --> A

In TOML, this looks like multiple [[actions.triggers]] blocks under the same [[actions]]:

# This action requires ALL THREE triggers to be true

[[actions]]

type = "open_long"

amount = "100 USDC"

[[actions.triggers]]

indicator = "rsi_14"

operator = "<"

target = "30"

timeframe = "1h"

[[actions.triggers]]

indicator = "sma_50"

operator = ">"

target = "sma_200"

timeframe = "1d"

[[actions.triggers]]

type = "price_change"

value = "-3%"

timeframe = "1h"

There is no OR logic within a single action. If you want "buy when RSI < 30 OR price drops 5%," create two separate actions -- one with the RSI trigger, one with the price drop trigger. Each action fires independently.

The max_count Field

Every trigger type supports an optional max_count field. It limits how many times that trigger can fire per position.

[[actions.triggers]]

type = "pos_price_change"

value = "-2%"

max_count = 1

max_count value | Behavior |

|---|---|

Not set (or None) | Trigger can fire unlimited times per position |

1 | Trigger fires once per position, then is disabled for that position |

3 | Trigger fires up to 3 times per position |

This is essential for DCA (Dollar-Cost Averaging) strategies where you want layered entries. Without max_count, a DCA trigger at -2% would keep firing every time the price bounces back and forth across the -2% threshold. With max_count = 1, it fires once, and you rely on the next DCA level (-4%, -6%) to add more capital.

A common pattern is to set max_count = 1 on each DCA level so each level fires exactly once per position. This prevents accidental double-buying at the same price level.

How Triggers Reset

Trigger fire counts reset when a new position opens. If a trigger on a DCA action has max_count = 1 and it fires once during Position A, that counter goes back to zero when Position A is closed and Position B is opened later.

The lifecycle looks like this:

graph TD

A["Position opens"] --> B["Triggers active<br/>fire counts = 0"]

B --> C{"Trigger<br/>conditions met?"}

C -- "Yes" --> D["Action fires<br/>fire count += 1"]

D --> E{"fire count<br/>< max_count?"}

E -- "Yes" --> C

E -- "No (or max_count reached)" --> F["Trigger disabled<br/>for this position"]

C -- "No" --> G["Wait for<br/>next evaluation"]

G --> C

F --> H["Position closes"]

H --> I["All fire counts<br/>reset to 0"]

I --> A

max_count is tracked per trigger, per position. If you have two separate actions each with their own -2% trigger and max_count = 1, each of them fires independently -- you would get two buys at the -2% level. Make sure your DCA levels are on separate actions with distinct thresholds.

Putting It All Together

Here is a minimal strategy that demonstrates all three trigger types working together:

[meta]

name = "Triggers Overview Demo"

description = "Shows all three trigger types in one strategy"

max_open_positions = 2

# ENTRY: open when RSI is oversold (Technical)

[[actions]]

type = "open_long"

amount = "100 USDC"

[[actions.triggers]]

indicator = "rsi_14"

operator = "<"

target = "30"

timeframe = "1h"

# DCA: buy more if position drops 3% (PriceChange)

[[actions]]

type = "buy"

amount = "100 USDC"

average_price = true

[[actions.triggers]]

type = "pos_price_change"

value = "-3%"

max_count = 1

# ACCUMULATE: buy on every 4h candle close (NextCandle)

[[actions]]

type = "buy"

amount = "25 USDC"

average_price = true

[[actions.triggers]]

type = "next_candle"

timeframe = "4h"

max_count = 5

# EXIT: sell when position is up 2% (PriceChange)

[[actions]]

type = "sell"

amount = "100%"

[[actions.triggers]]

type = "pos_price_change"

value = "2%"

This strategy opens a position when RSI dips, adds to it on dips and on a schedule, and exits at +2% profit. The max_count values prevent runaway accumulation: the DCA fires once, and the scheduled buys stop after 5 candles.

Continue reading the dedicated chapters for each trigger type to learn all the available fields and see more examples.

Technical Indicator Triggers

Technical triggers compare an indicator's current value against a target. They answer questions like "is RSI below 30?", "did the 50-day SMA just cross above the 200-day SMA?", or "is price above the upper Bollinger Band?"

These are the most common triggers in any strategy. If you have used TradingView alerts or any charting tool, you will recognize the logic immediately.

Anatomy of a Technical Trigger

A technical trigger has four fields:

[[actions.triggers]]

indicator = "rsi_14" # What to measure

operator = "<" # How to compare

target = "30" # What to compare against

timeframe = "1h" # On which candle timeframe (optional)

max_count = 1 # How many times it can fire per position (optional)

| Field | Required | Description |

|---|---|---|

indicator | Yes | The indicator to read. Format: type_period (e.g., rsi_14, sma_50, ema_200) or a special name (bb_lower, macd_line, price, ttm_trend). |

operator | Yes | How to compare the indicator to the target. One of: >, <, =, cross_above, cross_below. |

target | Yes | The value to compare against. Either a number ("30", "0", "-3") or another indicator ("sma_200", "bb_upper", "price"). |

timeframe | No | Which candle timeframe to evaluate on: 1m, 5m, 15m, 1h, 4h, 1d. If omitted, uses the session's default timeframe. |

max_count | No | Maximum number of times this trigger can fire per position. Omit for unlimited. |

Available Indicators

All of these can be used in the indicator field or as a target:

| Indicator | Format | Example | Description |

|---|---|---|---|

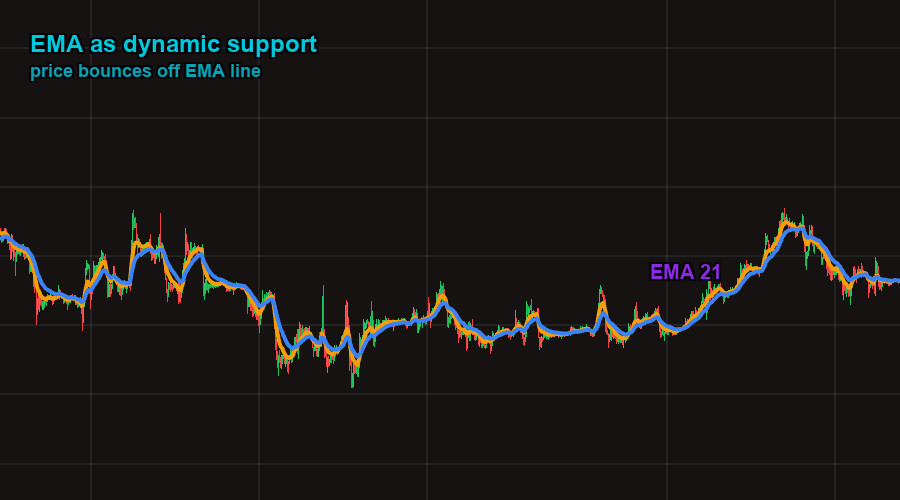

| SMA | sma_{period} | sma_50, sma_200 | Simple Moving Average |

| EMA | ema_{period} | ema_9, ema_21, ema_200 | Exponential Moving Average |

| RSI | rsi_{period} | rsi_14, rsi_7 | Relative Strength Index (0-100) |

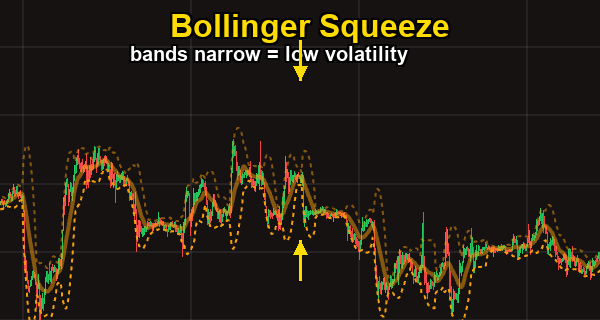

| Bollinger Bands | bb_{band} | bb_lower, bb_upper, bb_middle | Bollinger Band levels |

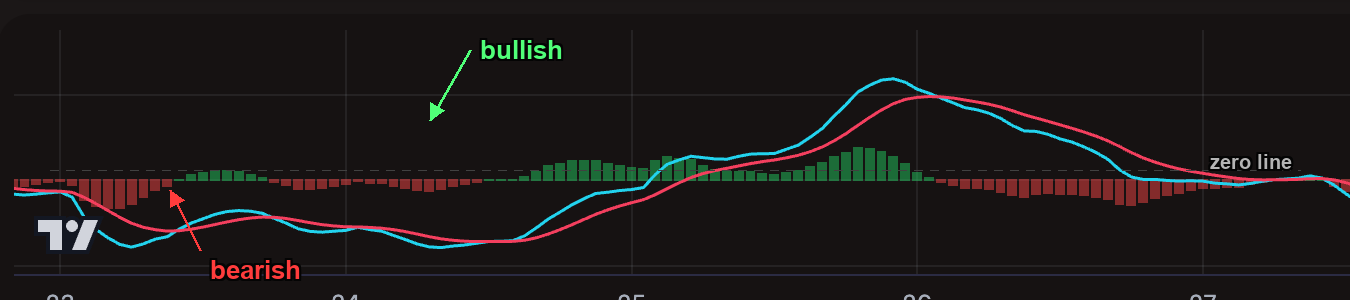

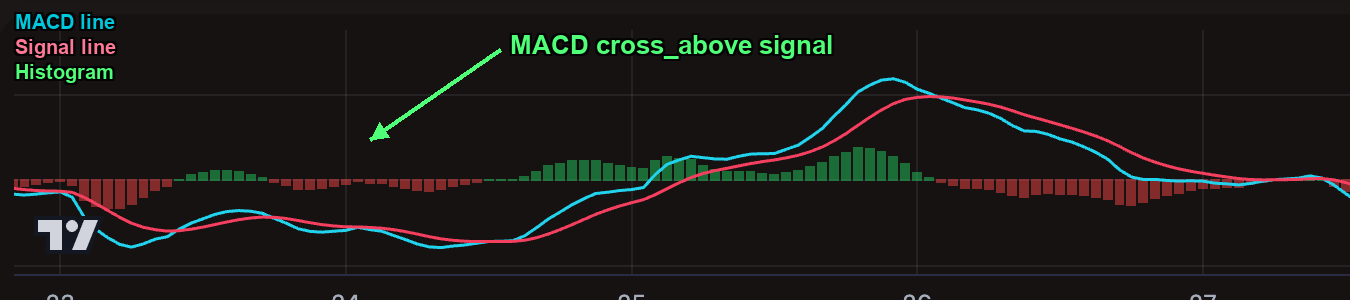

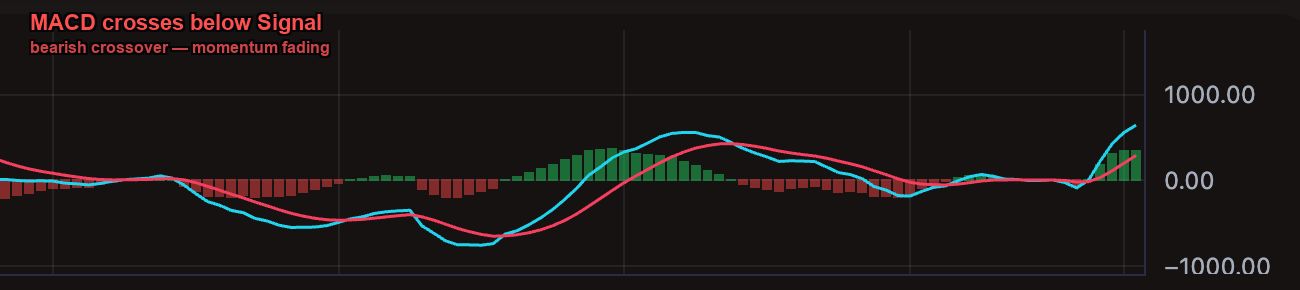

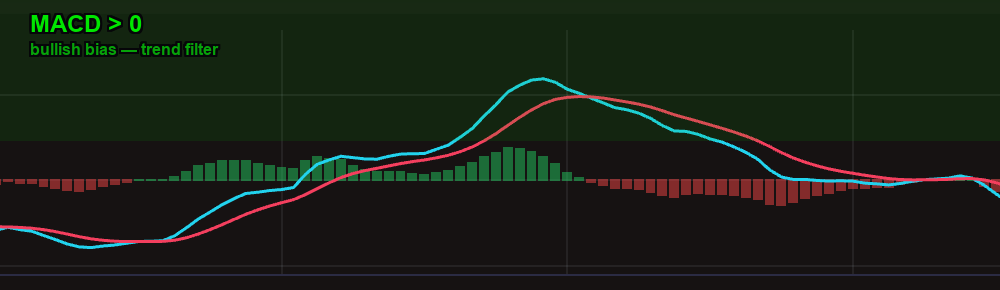

| MACD | macd_{component} | macd_line, macd_signal, macd_histogram | MACD components |

| StochRSI | stoch_rsi_{period} | stoch_rsi_14 | Stochastic RSI (0-100) |

| ROC | roc_{period} | roc_10 | Rate of Change (%) |

| ATR | atr_{period} | atr_14 | Average True Range |

| OBV | obv | obv | On-Balance Volume (no period) |

| OBV SMA | obv_sma_{period} | obv_sma_20 | SMA of On-Balance Volume |

| Volume SMA | vol_sma_{period} | vol_sma_20 | SMA of Volume |

| TTM Trend | ttm_trend | ttm_trend | TTM Squeeze trend (1 = bullish, -1 = bearish) |

| Price | price | price | Current market price (close) |

Operators Explained

> (Greater Than) and < (Less Than)

Simple threshold comparisons. The trigger is true whenever the indicator is above or below the target value.

# True whenever RSI(14) is below 30

[[actions.triggers]]

indicator = "rsi_14"

operator = "<"

target = "30"

These fire on every candle where the condition is true, not just the moment it crosses the threshold. If RSI stays below 30 for ten candles, the trigger is "active" on all ten. (Use max_count if you only want it to fire once.)

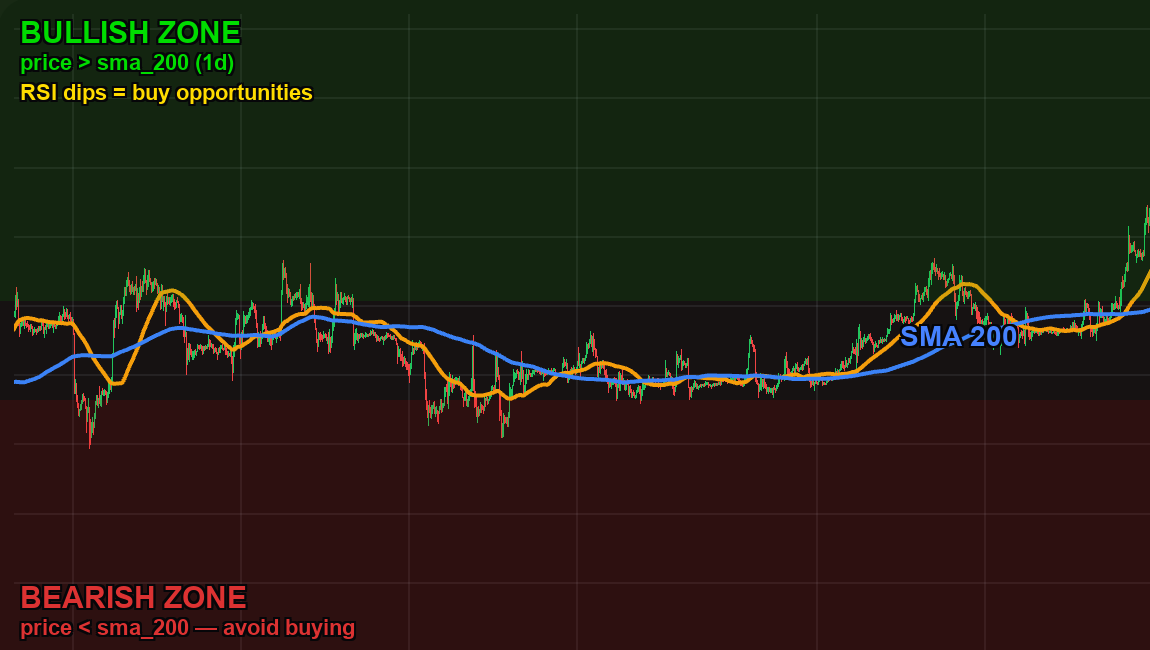

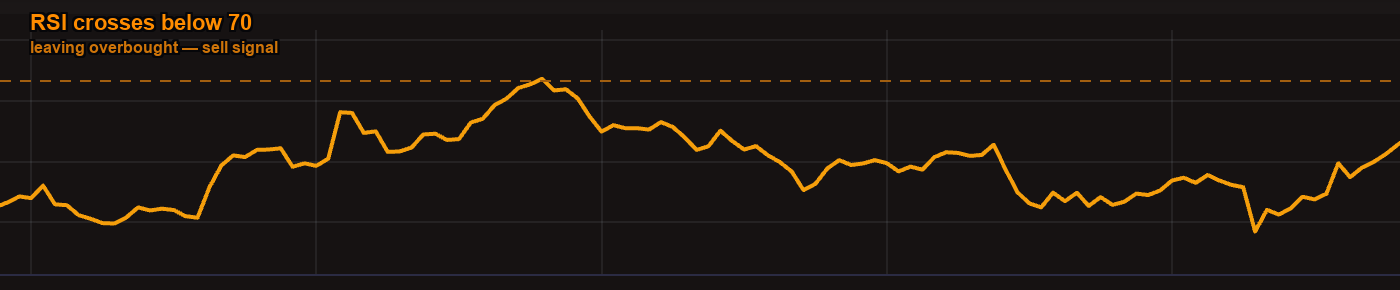

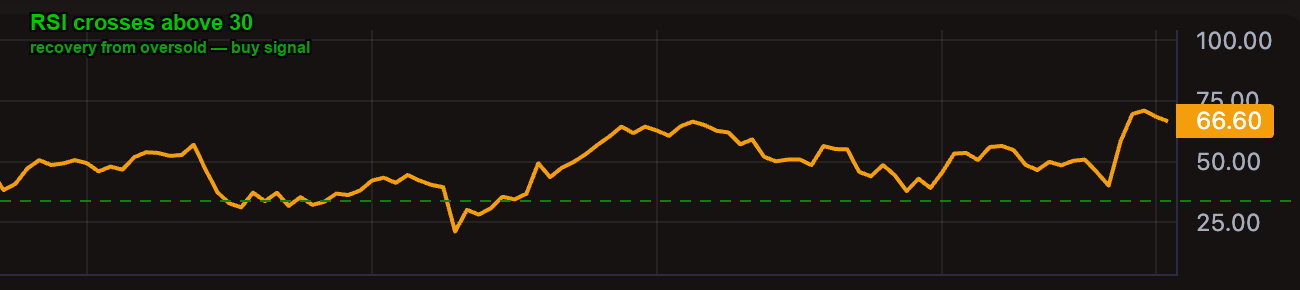

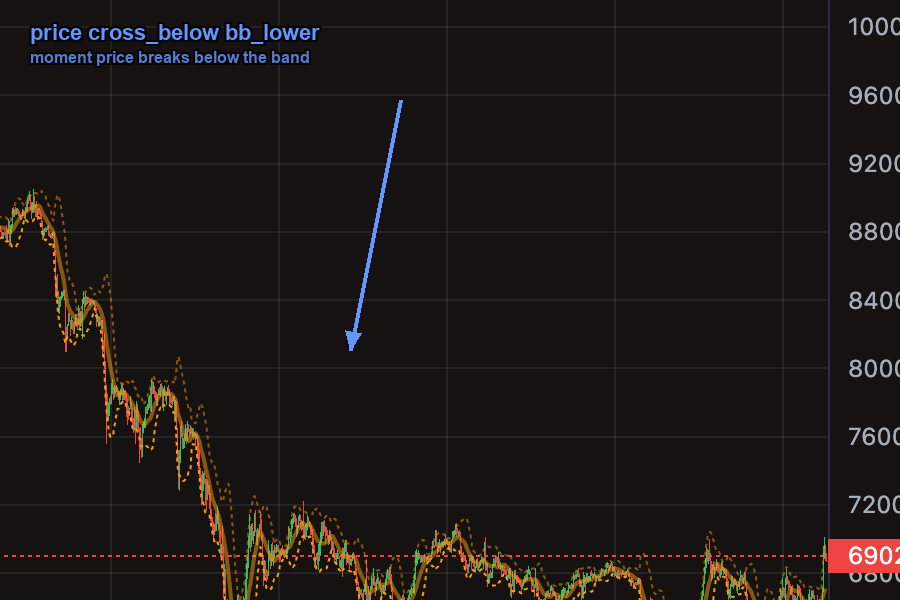

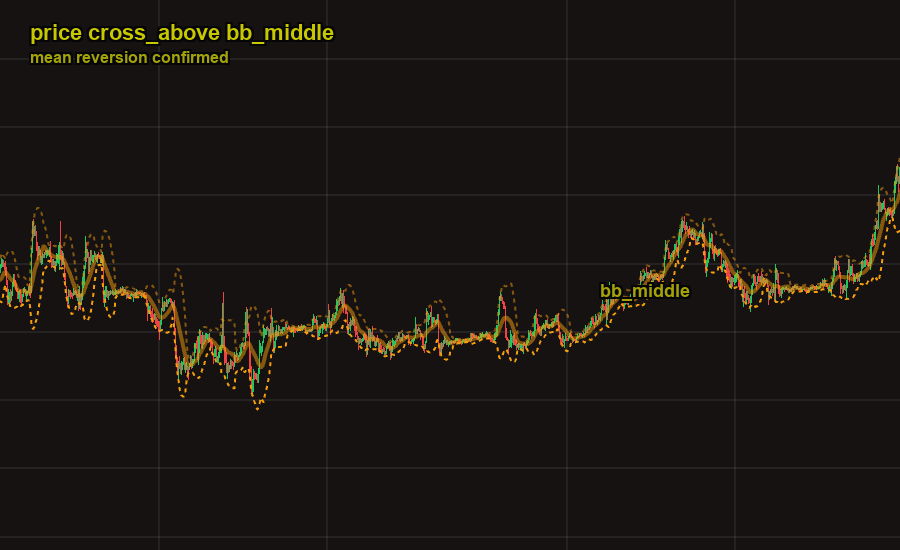

cross_above and cross_below (Crossover Detection)

A crossover trigger fires at the moment of transition. It checks two consecutive candles:

cross_above: The indicator was at or below the target on the previous candle, and is above it on the current candle.cross_below: The indicator was at or above the target on the previous candle, and is below it on the current candle.

graph LR

subgraph "cross_above"

P1["Previous candle:<br/>SMA(50) <= SMA(200)"]

C1["Current candle:<br/>SMA(50) > SMA(200)"]

P1 -->|"transition"| C1

end

subgraph "cross_below"

P2["Previous candle:<br/>SMA(50) >= SMA(200)"]

C2["Current candle:<br/>SMA(50) < SMA(200)"]

P2 -->|"transition"| C2

end

# Golden cross: SMA(50) crosses above SMA(200)

[[actions.triggers]]

indicator = "sma_50"

operator = "cross_above"

target = "sma_200"

timeframe = "1d"

Use cross_above and cross_below instead of > and < when you want to catch the turning point rather than the sustained condition. A golden cross (sma_50 cross_above sma_200) fires once when the trend shifts bullish, rather than on every single candle where SMA(50) happens to be above SMA(200).

= (Equal)

Exact match comparison. This is rarely used because indicator values are continuous floating-point numbers and exact equality is unlikely. The primary use case is the TTM Trend indicator, which outputs discrete integer values: